A 30-year-old tax provision could be discouraging 13.1 million Americans from selling their homes, lest they face a whopping tax bill on their profits when they want to sell.

New data from the National Association of Realtors® shows 15% of all owner-occupied households nationwide could face a major tax bill if they sell their homes. That’s because their expected profit from a sale has risen above the exemption for federal capital gains tax, which hasn’t been updated since 1997.

The median home price in 1997 was $129,000. Today, it’s $419,300, but the law still caps the tax exemption for home sellers at a $500,000 profit for couples, or $250,000 for an individual.

“The capital gains exclusion was established in a housing market with lower prices, shorter ownership tenures, and less cumulative appreciation than exists today,” NAR said in the report.

NAR says the provision needs updating to keep pace with inflation. The group argues that the potential tax hit from a sale may especially discourage older homeowners from downsizing, contributing to a national housing supply shortage.

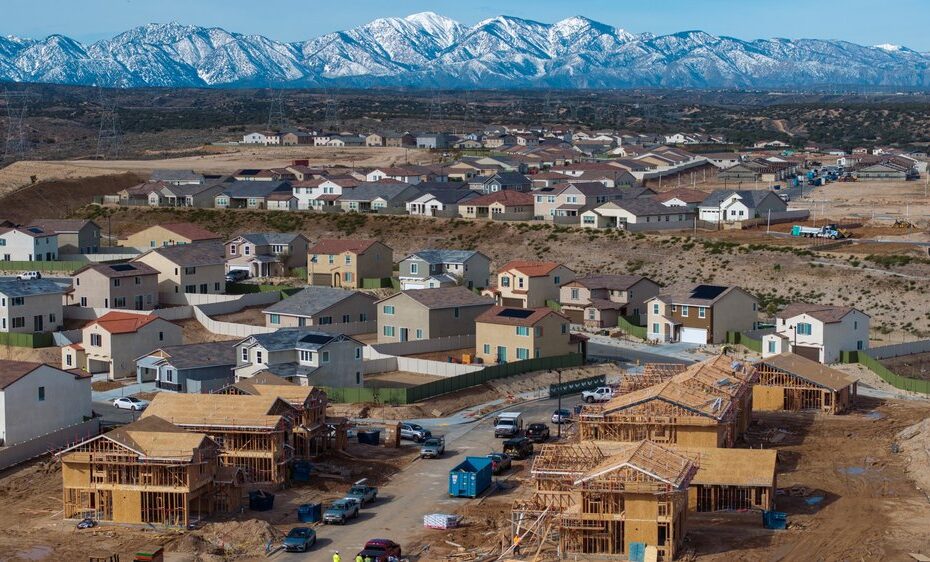

That would be unwelcome pressure for the housing market, which is already facing a housing shortage of millions of units. Younger buyers are overwhelmingly pessimistic they’ll ever afford homes given today’s market.

Growing concern

The current capital gains scheme, imposed in 1997, lets sellers exclude up to $250,000 in profit if single, or $500,000 if married and filing jointly, when they sell a primary home, with few strings attached.

But Congress didn’t tie the exclusion to inflation. For those homeowners who live in their properties longer, there may be a growing tax burden once they sell. And that impacts housing inventory in areas with the fastest-growing home prices.

Last year, NAR estimated that 1 in 3 homeowners could have built up more home equity than the capital gains exclusion. It expected that number would grow to 56% by 2030.

Now, NAR’s research finds 25.4 million homeowners hold prospective profit gains over $250,000, and 8 million over $500,000.

Homes have steadily increased in value in the West and Northeast, so there are big concentrations of homeowners potentially “locked in” by taxes in those areas. California, Idaho, Utah, Arizona, and Nevada are among areas with fast-rising home values. Many homeowners in those states could soon cross the threshold and face a tax hit.

The Midwest and parts of the South have lower exposure. But the trend is the same even in those affordable markets, NAR said.

Realtor.com® senior economist Joel Berner said the 30-year-old exemption limit complicates housing market dynamics, especially as baby boomers and the Silent Generation, who control 29.6 million homes of $13.8 trillion in home value, consider what to do with their real estate.

“This is an outdated figure that is keeping homeowners who have been in place for a long time and seen major home value appreciation from selling,” Berner said. “Boosting this exclusion would help free up some long-locked-up inventory.”

Chipping away

At a January NAR event, several policy experts dissected the challenges of altering the limit, which could have major implications on tax revenue for the federal budget. President Donald Trump previously said he was in favor of a change.

Michael Kelley, senior director of the Bipartisan Policy Center, said at the NAR event that a targeted measure, for example aimed at older adults hoping to downsize, is smarter. They are locked in to homes where they raised their children, and where new young families want to buy.

Lawmakers have pitched increasing the limit a few times. But any change to the limit means a major hit to government revenue. And it’s not clear raising the limit will soften every market.

“It could help some of these first-time homebuyers who are eligible and ready to get into the market,” Kelley said. “It probably doesn’t work in every city, every county, every state.”

Rep. Jimmy Panetta, a California Democrat on the House Ways and Means Committee, wants to double the limit. He’s brought 119 co-sponsors to his More Homes on the Market Act. But that bill remains in committee.

Virginia Rep. John McGuire, a Republican, introduced a bill Jan. 14 that would let seniors exclude home sales to first-time homebuyers from capital gains. Ten Republicans co-sponsored that measure, H.R. 7051. It too remains in committee.