The traditional spring homebuying season has officially arrived, injecting seasonal optimism into a market that has struggled in the face of economic uncertainty.

While real estate experts have identified the current week as the premier window for sellers to list their homes, new data from Realtor.com® shows a market defined by cooling sales, shifting buyer-seller dynamics, and a historic “lock-in” effect that continues to weigh on the market.

According to an analysis by Realtor.com, the week of April 12–18 represents the “Best Time To Sell” for the United States at large. This optimal window extends to 12 major metropolitan areas, including Atlanta, Dallas, and Detroit.

For homeowners in Florida markets such as Orlando and Tampa, the ideal conditions are expected to peak next week, April 19–26.

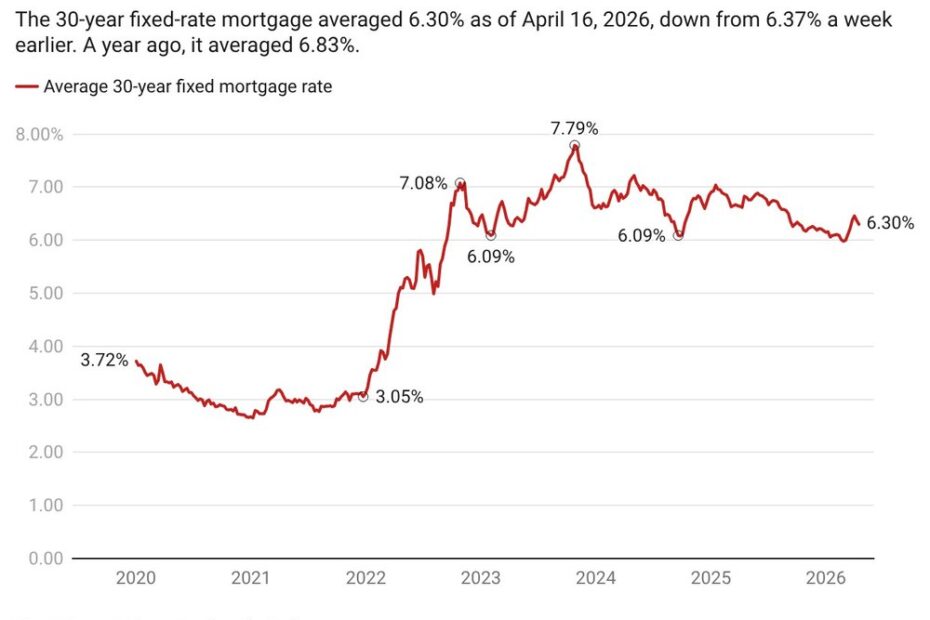

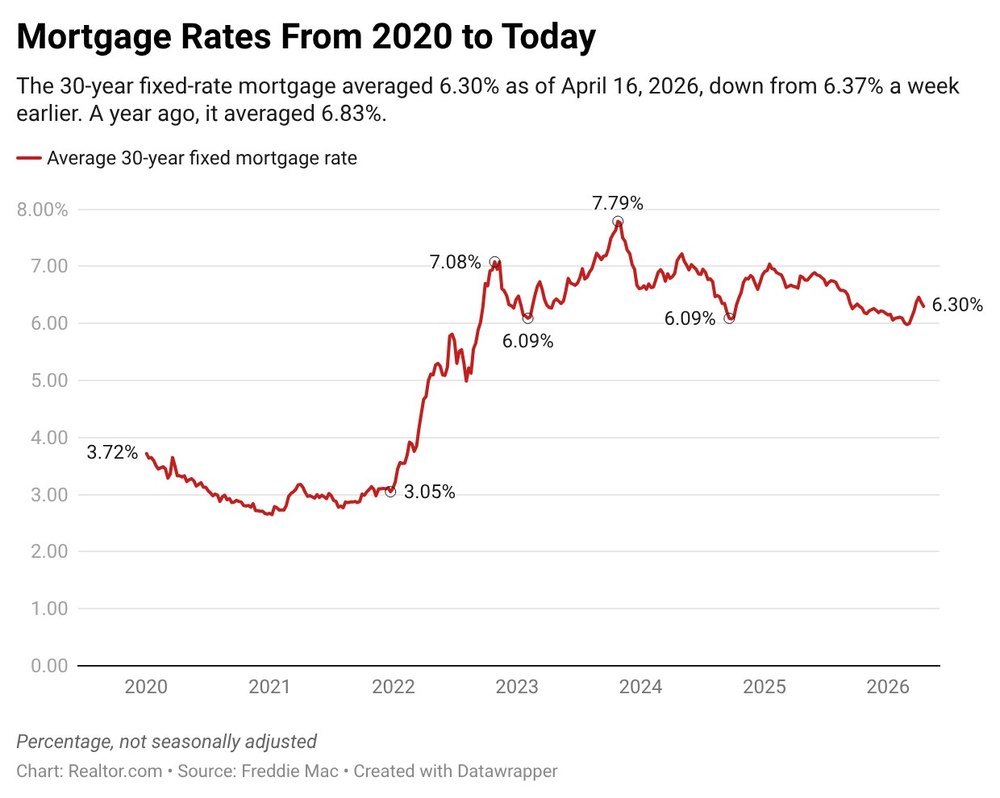

Despite this seasonal “green light,” the broader data suggests a sluggish start to the spring. March existing-home sales fell by 3.6% from February, landing at a seasonally adjusted annual pace of 3.98 million. This decline occurred despite mortgage rates hitting a multiyear low in late February—a dip that typically fuels a sales boost in the following month.

A significant hurdle for the 2026 market remains the “lock-in” effect. For the first time in history, the share of outstanding mortgages less than 4 years old has plummeted to just 32.1%, nearly 20 points below the long-term average.

The gap between interest rates on outstanding mortgages and today’s market rates remains quite high. This disparity has discouraged homeowners from trading up, effectively freezing inventory.

Furthermore, the financial burden on homeowners is reaching new heights. By the end of 2025, the average monthly payment on outstanding mortgages topped $2,000 for the first time.

The power balance between buyers and sellers is also becoming increasingly localized. The inaugural Market Clock Report indicates that the U.S. housing market is more fragmented than it has been in years. While 40% of prospective sellers still believe the market favors them, a significant 60% now view the market as either balanced or favoring buyers.

This shift in sentiment is manifesting in seller behavior. While nearly 84% of sellers expect to receive at least their full asking price, roughly 39% now anticipate having to make concessions to close the deal—a notable increase from 30.2% last year.

For those currently priced out of a purchase, the short-term financial math continues to favor the rental market. In all 50 of the largest U.S. metros, renting remains the more affordable monthly option, with renters saving an average of $920 per month compared to buyers.

However, certain regions, such as Washington, DC, are seeing that gap narrow. Experts suggest that while high costs persist, the current dip in rental prices provides a strategic window for future buyers to increase their down payment savings while they wait for more favorable conditions later in the year.