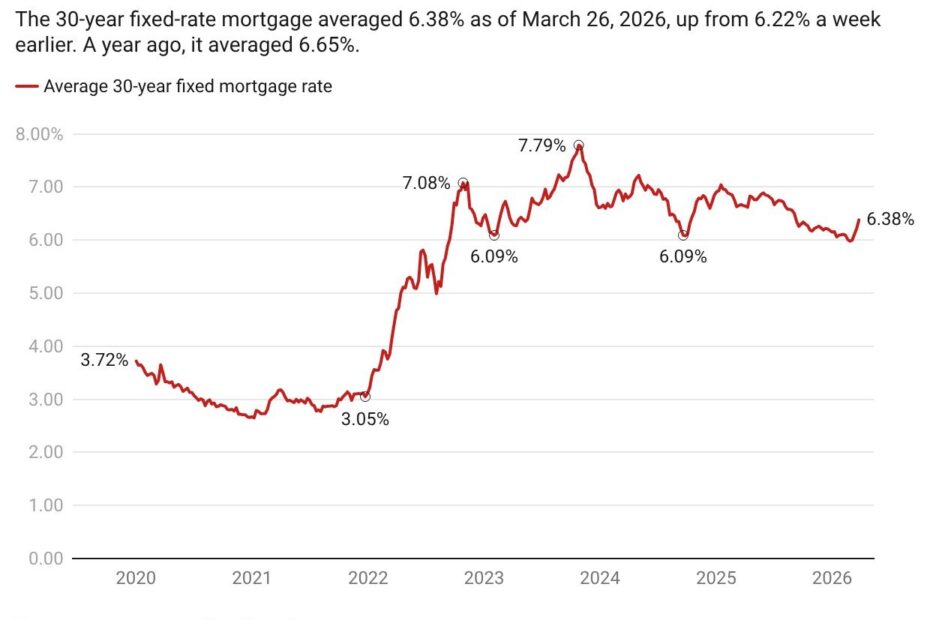

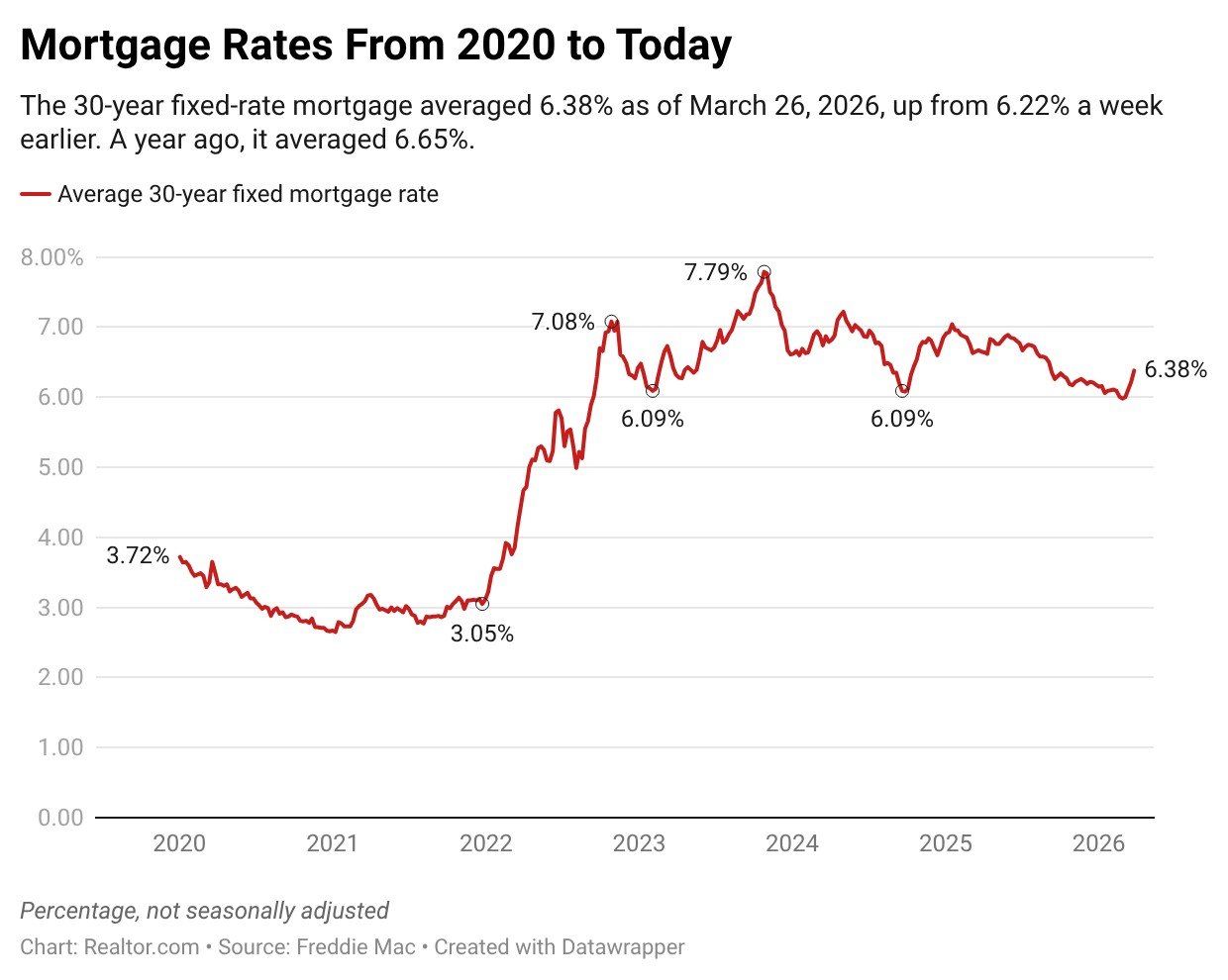

Mortgage rates jumped 16 basis points last week, their largest single-week increase in nearly a year, putting additional pressure on homebuyers already navigating a challenging market.

The three-week climb marks the steepest such rise in more than a year and a half, according to Freddie Mac data.

The rate spike is compounding affordability pressures for buyers. Higher rates are eroding purchasing power at the same time that rising oil prices are weighing on consumer confidence, creating a squeeze from multiple directions.

While rates remain below where they stood a year ago, many home shoppers have had to recalibrate their budgets—a shift that is expected to dampen sales activity in the months ahead.

Sellers are adjusting expectations

Despite the headwinds for buyers, new data shows some encouraging signs on the supply side. Sellers entering the market appear to be moderating their price expectations, with the typical asking price running nearly 2% below year-ago levels. New listings, however, have fluctuated from week to week, limiting how much buyers can benefit from the softer pricing.

Total inventory continues to rise as homes sit on the market longer, reflecting a degree of patience among buyers who appear to be in no rush to close.

The best time to sell is almost here

The timing of all this matters. Spring carries an outsized influence on the housing market, as a seasonal uptick in shopping activity historically tilts conditions in sellers’ favor. Nationally, the best time to sell is the week of April 12–18, 2026, according to Realtor.com® senior economic research analyst Hannah Jones.

But sellers in several markets don’t need to wait that long. The optimal window to list in Cincinnati, Seattle, and Grand Rapids, MI, arrives next week, March 29–April 4. Just recently, 16 markets hit their peak seasonal timing this week, March 22–28.

Luxury housing, mobile homes, and renters: What new research shows

The Realtor.com economic research team has released three reports that shed additional light on different corners of the housing market.

Raleigh and Washington, DC: A Luxury Connection

Senior economist Anthony Smith examines the luxury housing markets in Raleigh-Cary, NC, and the Washington, DC, metro area. Beyond geographic proximity, both markets share a foundation in knowledge-work industries. That connection shows up in the data: The DC metro area ranks as the top source market for out-of-town home shoppers looking at properties in Raleigh-Cary.

Mobile Homes: Lower Cost, Uneven Distribution

Senior economist Joel Berner‘s report finds that mobile homes represent a more affordable—if less common—housing option across the country. They are concentrated in nonmetro areas and warmer climates, with notable concentrations in Florida and the Southwest.

Who’s Renting—and Why Affordability Is the Common Thread

Economist Jiayi Xu breaks down today’s renter population into three major groups: young households (31.9%), family households (44.3%), and long-term renters (36.1%). Together, with some overlap across categories, these groups account for more than 80% of all renter households. Across all three, affordability emerges as the defining challenge.

Young households are gravitating not toward major metros but to midsized cities—Colorado Springs, CO, Austin, TX, and Denver top the list—where rents are more manageable and the need for roommates is lower.

Family households are concentrated in majority-minority markets across California, Texas, and Florida, where affordability is under the most strain.

Markets like McAllen, TX, Stockton, CA, Bakersfield, CA, Riverside, CA, Miami, and Honolulu rank among the highest for family renter share.

Generational wealth plays a role, as homeownership rates among minority households remain lower and the financial benefits of owning are passed down less often.

Long-term renters cluster in rent-regulated cities like New York City and Los Angeles, where stabilization policies can keep rents relatively affordable but may also limit residents’ ability—or incentive—to move.