More Americans are breaking into the upper middle class, but for those left behind, the dream of homeownership may be slipping out of reach.

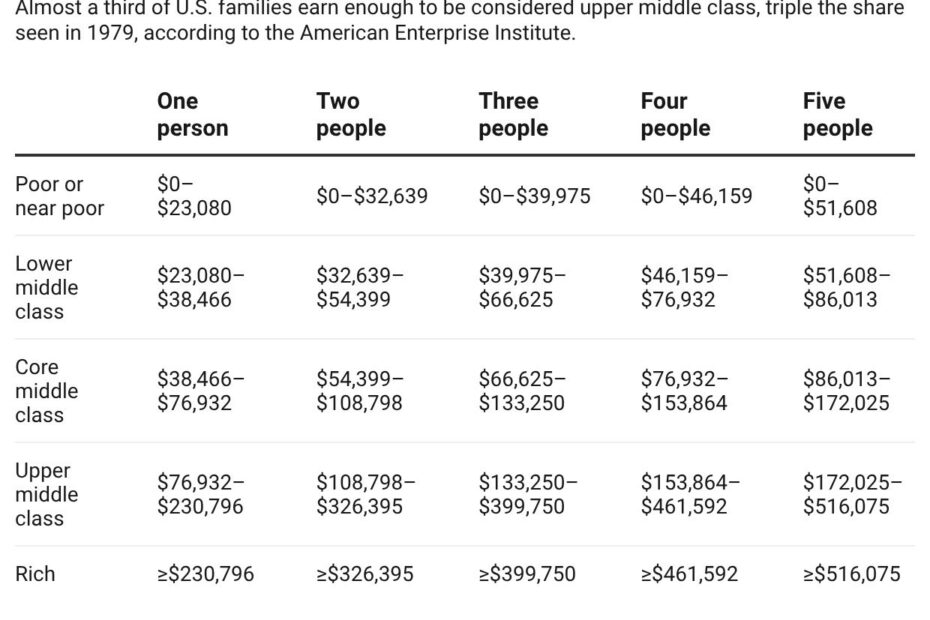

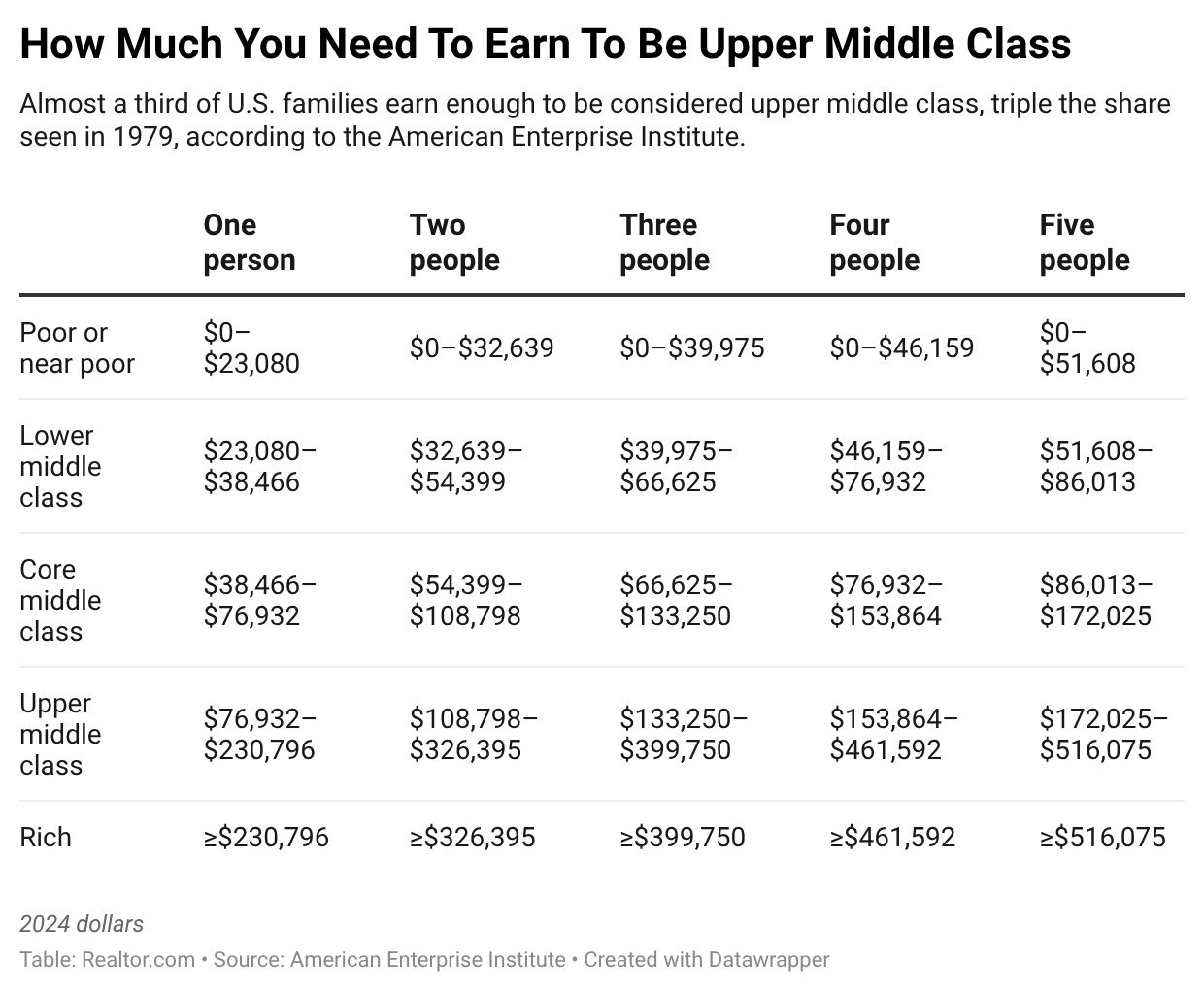

About 31% of U.S. households earn enough to be considered upper middle class, up from just 10% in 1979, making it the nation’s largest economic group, according to research from the American Enterprise Institute, a nonpartisan think tank.

Meanwhile, the share of Americans considered core middle class shrank just below 31%, down from 33% in 2001 and 36% in 1979. The population shares for those considered lower middle class and poor also shrank, indicating a broad trend toward upward mobility.

“American families up and down the income ladder have seen sizable gains over the past half century,” researchers Stephen J. Rose and Scott Winship wrote in the report. “Economic growth, greater professional opportunities for women, and a robust safety net have more than offset the decline of marriage. Claims that the middle class is ‘shrinking’—and especially that it has hollowed out—are not helpful for understanding changes in material well-being.”

Even so, data from Realtor.com® suggests that the typical middle-class family as defined in the report would struggle to afford the median-priced home in today’s America, raising questions about living standards for those who haven’t ascended to the upper middle class.

Although there are no universal definitions of class in America, the AEI report uses household income, defining the upper middle class as a family of four earning between $153,864 and $461,592 per year.

Meanwhile, a family of four would be middle class if they earned between $76,932 and $153,864 annually, according to the report’s definition.

The report doesn’t factor in the wide range in the cost of living in different parts of the country. For example, $76,932 goes a lot further in Peoria, IL, than in San Jose, CA. Rather, it looks at national averages over time to measure overall changes in Americans’ income and living standards.

Although the report does not address housing costs, a Realtor.com analysis suggests that the middle-class families described in the report might struggle to afford a home in today’s market.

In March 2026, the typical four-bedroom home in America cost about $516,000. With a 10% down payment at today’s mortgage rate of 6.46%, a household would need to earn at least $146,500 a year to comfortably afford it.

That would put the typical four-bedroom home in easy reach for an upper-middle-class family of four, but excludes most of the middle-class category.

“For a typical middle-class family, a median-priced four-bedroom home is largely out of reach by conventional financial standards,” says Realtor.com senior economic research analyst Hannah Jones. “Affording one likely means buying smaller, choosing a lower-cost market, or putting more money down to reduce monthly payments.”

Meanwhile, the typical three-bedroom home requires an income of $105,500 at today’s prices and rates. That would be attainable for about two-thirds of the middle-class income range, if a family of four has one shared bedroom and forgoes a guest bedroom or home office.

It suggests that although Americans overall are better off today than in the past, those considered middle class face bigger challenges in buying a home.

In 1979, the inflation-adjusted income for a middle-class family of four would have ranged from $21,863 to $43,725, according to AEI’s definition.

Yet, even with mortgage rates above 11%, the median-priced home in 1979 required an annual income of just $25,500, putting it within reach of nearly all middle-class families. (Price data from 1979 does not include the number of bedrooms. However, the typical home of that era had about three bedrooms.)

It means that homeownership may be less characteristic of the middle-class lifestyle than in prior decades, even as overall standards of living have improved.

“Strong wage growth over the past several years hasn’t been enough to offset the surge in living costs that took hold in 2020 and never fully let up,” says Jones. “Housing has been a major driver of that squeeze, making it harder both to save for a down payment and to afford the monthly costs once you get there.”

That disconnect may help explain why some believe the American middle class is “hollowed out,” despite the convincing AEI research showing that overall incomes are rising. After all, if the typical middle-class family can’t afford a home, are they truly middle class?

“The gap between middle-class income and what it actually takes to buy a family home has grown wide enough that homeownership now effectively requires an upper-middle-class income,” says Jones.