We saw a softer-than-expected February jobs report, with unemployment rising and employers shedding more than 90,000 jobs.

One bright spot: Earnings growth continued, edging slightly higher. The softer report could mean more tension between the Fed’s two goals, especially if next week’s inflation readings are high. But I don’t expect it to change the March decision, and futures markets suggest that investors also expect the Fed to hold tight.

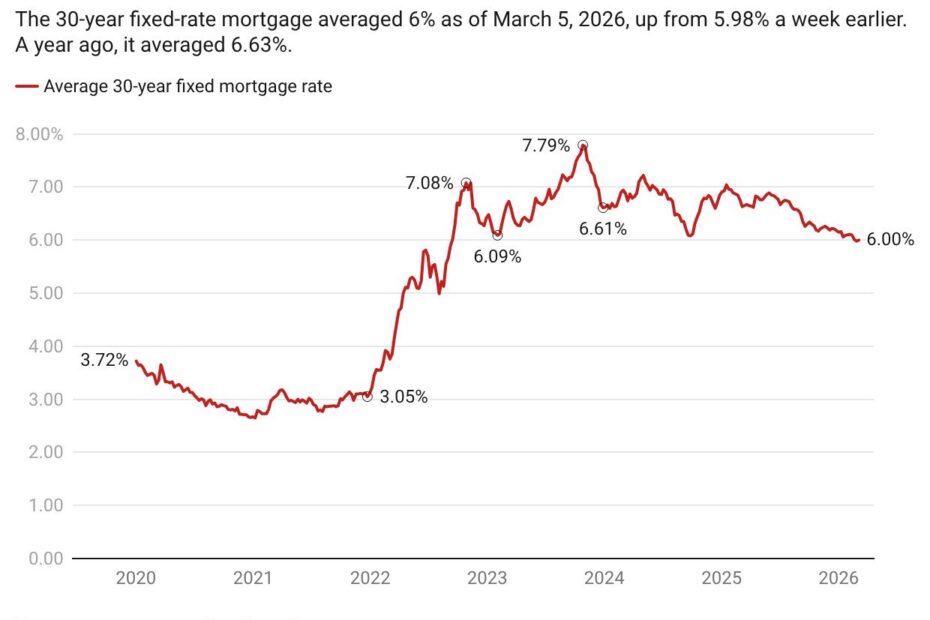

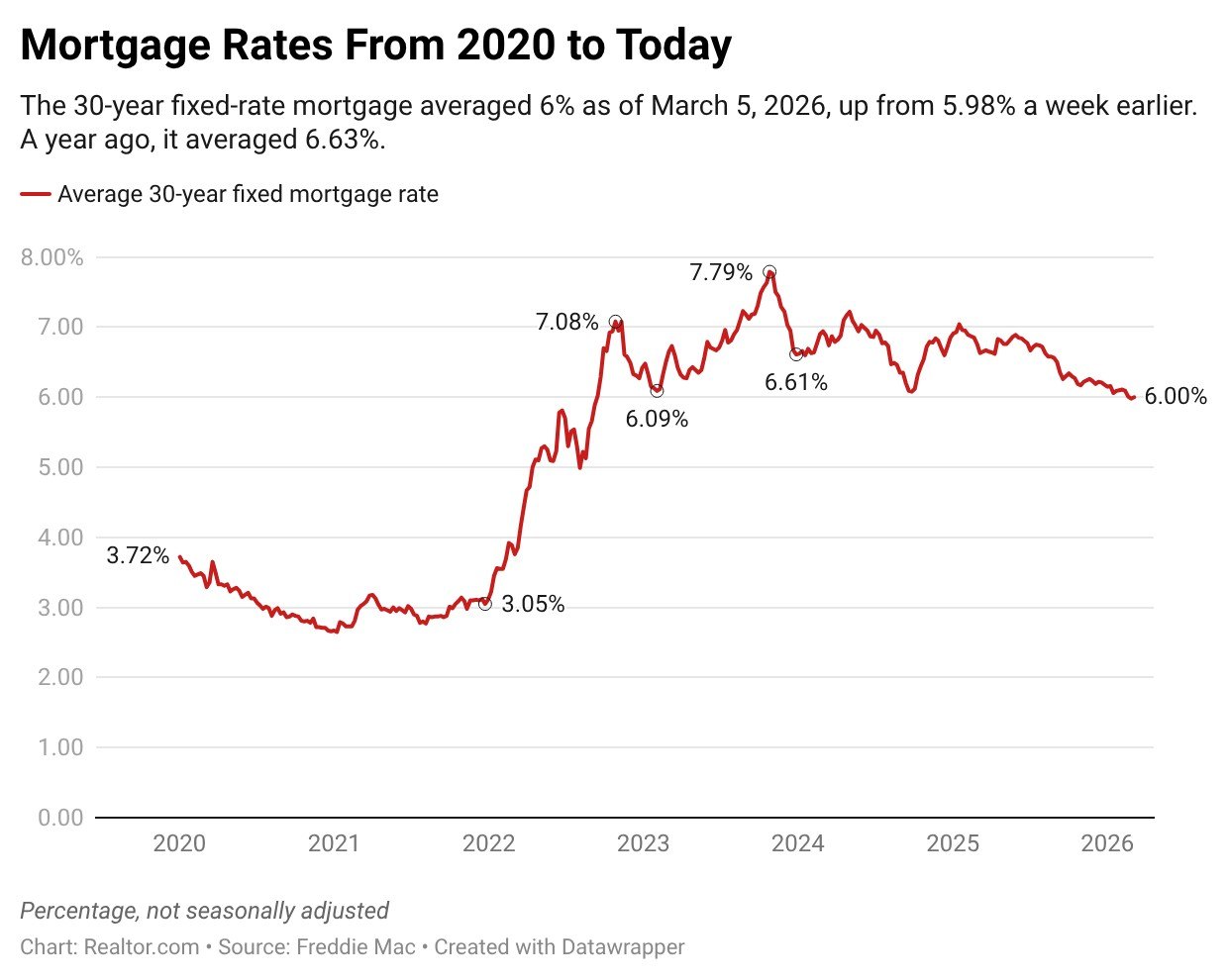

Last week, mortgage rates dipped below 6%, but this week, the conflict in Iran and inflation fears, which remain on edge in a higher-tariff rate world, have pushed 10-year yields higher. Mortgage rates ticked up to 6% and are likely to move higher unless we see de-escalation.

But it’s vital to keep these moves in context. Last year, mortgage rates were above 6.6% and climbed to nearly 6.9% in May. Put simply, mortgage rates are still quite a bit lower than last spring, and I expect them to remain lower, which sets up a nice housing market tailwind, even if we see further upticks.

The better mortgage rate environment is just one of several buyer positives. The Realtor.com® February Housing Trends report also showed that new listings climbed even as weather likely kept new listings lower in the Northeast.

But the overall increase in active for-sale listings continues to lose momentum, and gains have been concentrated in lower-priced tiers in the South and West. This is one of the factors nudging the typical listing price lower.

The report also examined data on contract cancellations, finding that the share of canceled contracts among homes on the market is in line with historic norms. Cancellations aren’t rare—so both buyers and sellers should keep this in mind as they negotiate—but our data suggests that they’re roughly as common as they usually are at this time of year.

Looking at Realtor.com housing data on trends in the past week shows that home price softness was steady throughout the month as active listings growth lost momentum. Fortunately, new listings grew for a third week and we are logging this growth as we move ever closer to the heart of selling season. This is a key indicator of buyer-seller momentum that I’m watching.

The reason new listings continue to be so important is that housing supply has not fully recovered from the COVID-19 pandemic shock that exacerbated the pre-existing shortage.

In fact, the Realtor.com 2026 Housing Supply Gap report found that the shortage widened somewhat last year and now sits just above 4 million homes nationwide. But it’s important to note that, relative to the recent pace of building, the South and West have much smaller gaps while the Northeast and Midwest see more acute housing shortages.

Finally, we took a look at two luxury markets in these short-supplied regions—Chicago and Philadelphia—and found that despite the nearly 800 miles separating these metropolises, their luxury markets look like mirror images.