Financial markets are now predicting that the Federal Reserve will not make any rate cuts in 2026, as policymakers grapple with potential economic fallout from the U.S.-Israel war with Iran.

On Monday, Fed Chair Jerome Powell addressed economic students at Harvard University, where he said that the oil price shock from the war would likely be temporary, but noted that it was too early to judge the war’s full impact.

“Now we’re facing events in the Middle East which will certainly affect gas prices, and we feel like our policy is in a good place for us to wait and see how that turns out,” said Powell. “Energy shocks have tended to come and go quickly. … So the tendency is to look through any kind of a supply shock.”

However, Powell noted that the latest turmoil follows multiple years of elevated inflation, saying it would be critical to monitor the oil shock’s duration and impact on inflation expectations among consumers and businesses.

“It’s one of those times where you get a series of supply shocks: first the pandemic, then the much smaller one from tariffs, and then we’re getting now an energy shock,” he said. “No one knows how big it will be. It’s way too early to know.”

Since the war began on Feb. 28, global oil prices have soared as shipping through the crucial Strait of Hormuz has all but halted. In the U.S., average gas prices have jumped roughly a dollar over the last month, and are quickly approaching $4 per gallon for regular gasoline, according to AAA.

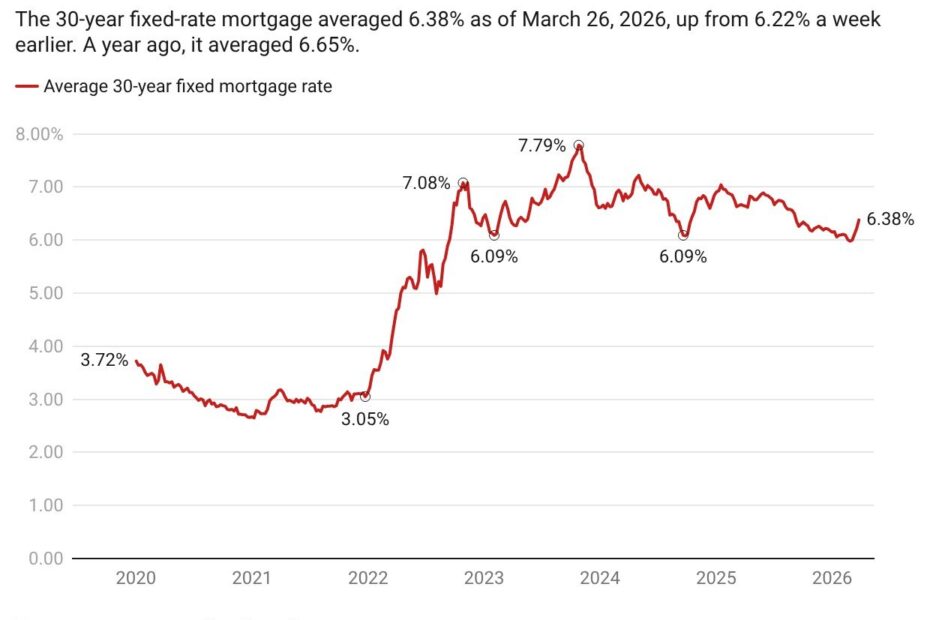

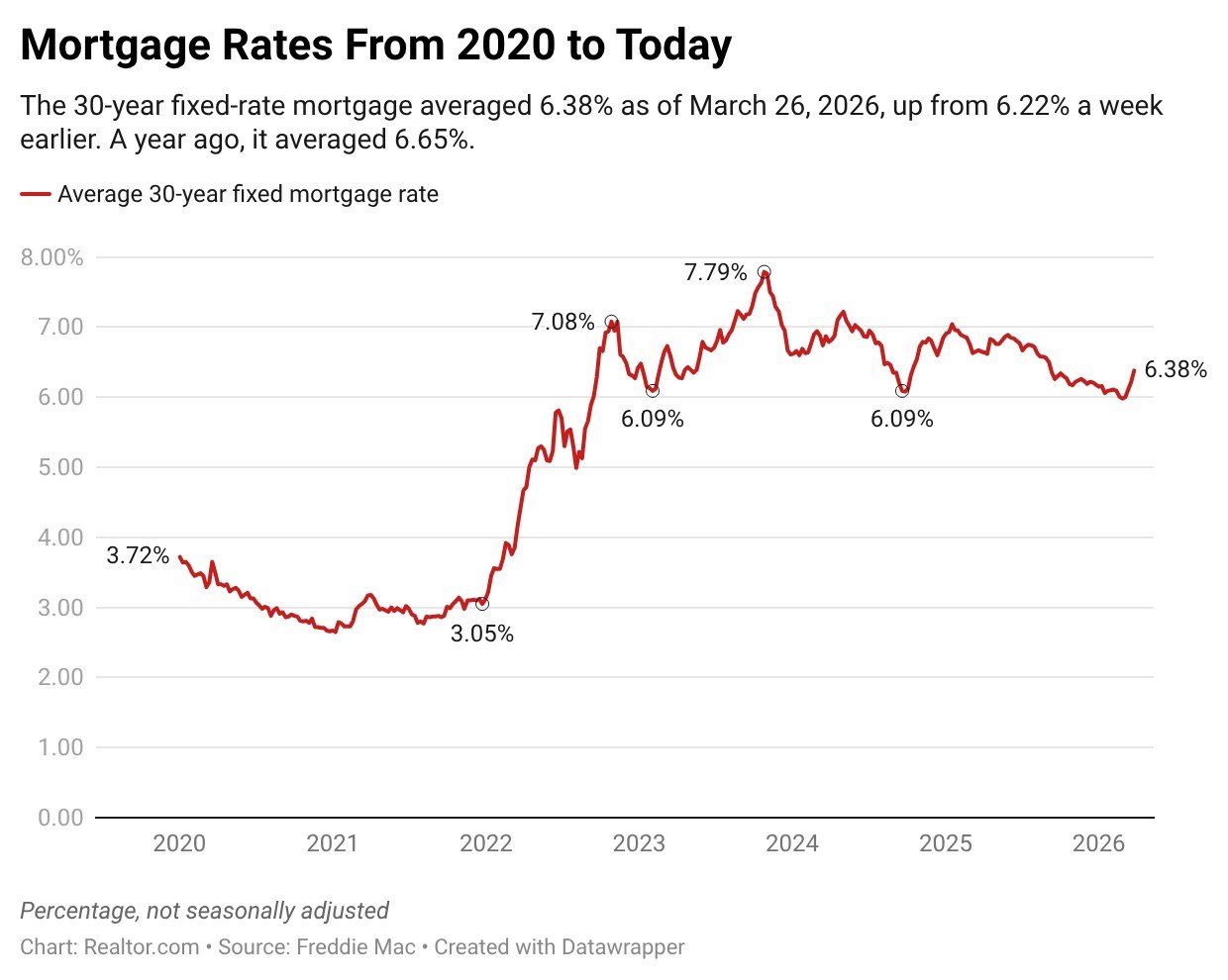

Those developments have sent mortgage rates up sharply, with rates averaging 6.38% last week, up from a three-year low of 5.98% in February, according to Freddie Mac.

Driving mortgage rates higher are concerns that the oil shock will spark renewed inflation, forcing the Fed to delay further interest rate cuts, or possibly raise rates to contain price increases.

The Fed uses higher interest rates to fight inflation, and lower rates to stimulate the labor market, in line with the central bank’s dual mandate of price stability and maximum employment.

Bond markets now assess a 77% probability that the Fed’s benchmark interest rate will be the same in December as it is today, in a range of 3.5% to 3.75%, according to CME Fedwatch. Before the war, markets had expected one or two rate cuts this year.

On the prediction marketplace Polymarket, traders saw a 34% chance that the Fed would make no rate cut in 2026, up from just 10% before the war began.

For now, Fed policymakers are telegraphing a “wait and see” message when it comes to the war’s impact on rate policy.

In comments last week, Fed Gov. Michael Barr, one of the 12 voting members on the rate-setting Federal Open Market Committee, said that it was too early to judge the war’s impact on inflation and the economy.

“If the conflict were to end soon, it is possible its effects on inflation and economic activity could be limited,” he said. “But if it continues for some time, the spike in energy prices and other commodities could have broader implications for both prices and economic activity.”

Barr noted that after five years of elevated inflation, yet another price shock could increase longer-term inflation expectations, which have the potential to become a self-fulfilling prophecy.

“Consumers and businesses factor future inflation into their current economic decisions, so there is a risk that this dynamic could lead to inflation persistence, making it more difficult to return inflation to 2%,” he said. “We need to be especially vigilant.”

Realtor.com® senior economist Jake Krimmel says the comments indicate that Fed policymakers remain cautious before simply dismissing the oil shock as a temporary supply issue.

“The trouble is this particular energy shock is not happening in a vacuum. First off, we don’t know how long it will last and we don’t know the knock-on effects to other fuel-reliant sectors. Second, the oil price spike is part of a larger supply side shock to global trade due to the issues with the Strait of Hormuz. And third, all of this is happening against a backdrop of concern over inflation expectations from our last episode of stress testing global supply chains: the tariffs,” says Krimmel.

Krimmel says that all indications point to the Fed keeping interest rates on hold until policymakers gain a deeper understanding of the impact on inflation, and until some uncertainty is resolved over the future of the conflict.

“Though the FOMC is always watching both sides of its dual mandate, they appear far more vigilant to the price stability side at the moment,” he says. “The hope is that this vigilant posture alone can keep consumer expectations and the bond market relatively anchored as they await new data and any new developments in Iran.”

For mortgage rates, movement in the 10-year Treasury yield will be key, as markets watch the fallout from the war and judge the likely impact on inflation.

Long-term bond yields, which closely correlate to mortgage rates, shot up after the war began. A prolonged oil shock and global energy crisis could send them higher, although a recession would have the opposite effect.

“Regardless, it does not look like 2026 will be the spring of the sub-6% mortgage,” says Krimmel.