Federal Reserve policymakers are keeping interest rates on hold, as the Iran war sends oil prices soaring and threatens to ignite a new round of inflation.

Fed Chair Jerome Powell joined the 11-1 majority on the Federal Open Market Committee to vote in favor of leaving the federal funds rate unchanged at Wednesday’s meeting in Washington, DC, judging inflation as a greater risk than weakness in the job market.

“The implications of developments in the Middle East for the U.S. economy are uncertain,” Powell said at a press conference. “Near-term measures of inflation expectations have risen in recent weeks, likely reflecting the substantial rise in oil prices caused by the supply disruptions in the Middle East.”

The lone dissent in Wednesday’s vote came from Fed Gov. Stephen Miran, who instead voted for a quarter-point rate cut, continuing his streak of dissents favoring lower interest rates since his appointment last year.

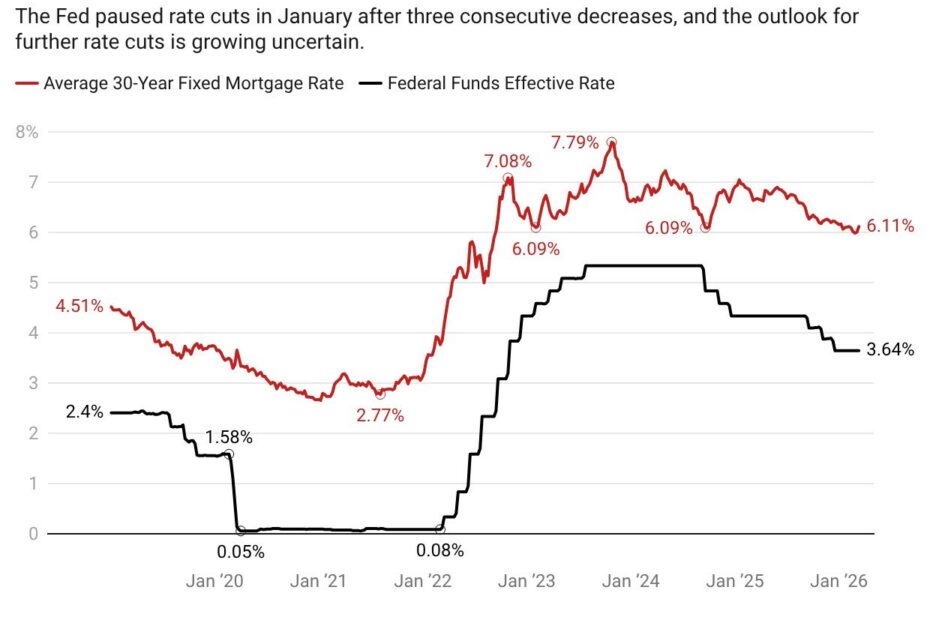

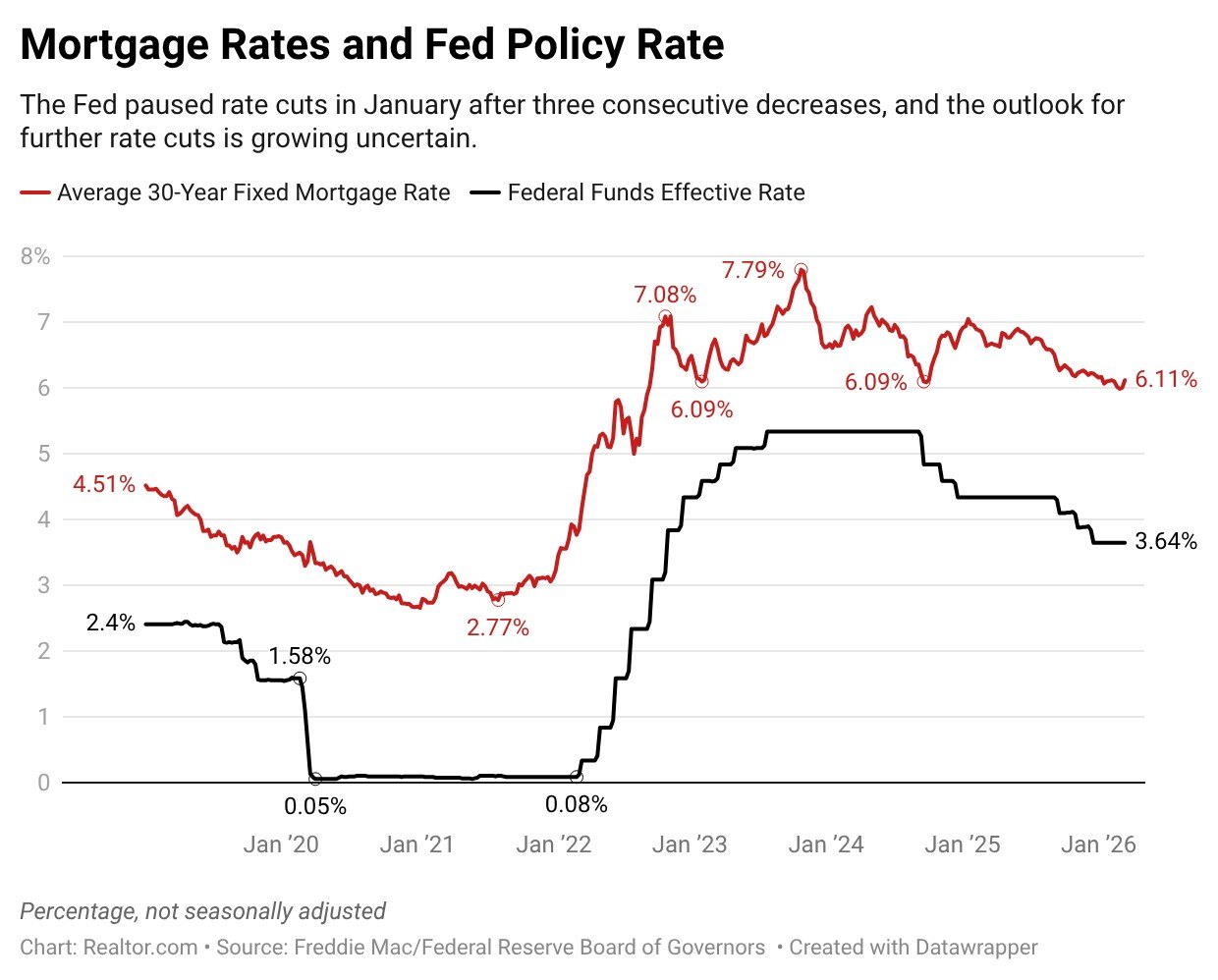

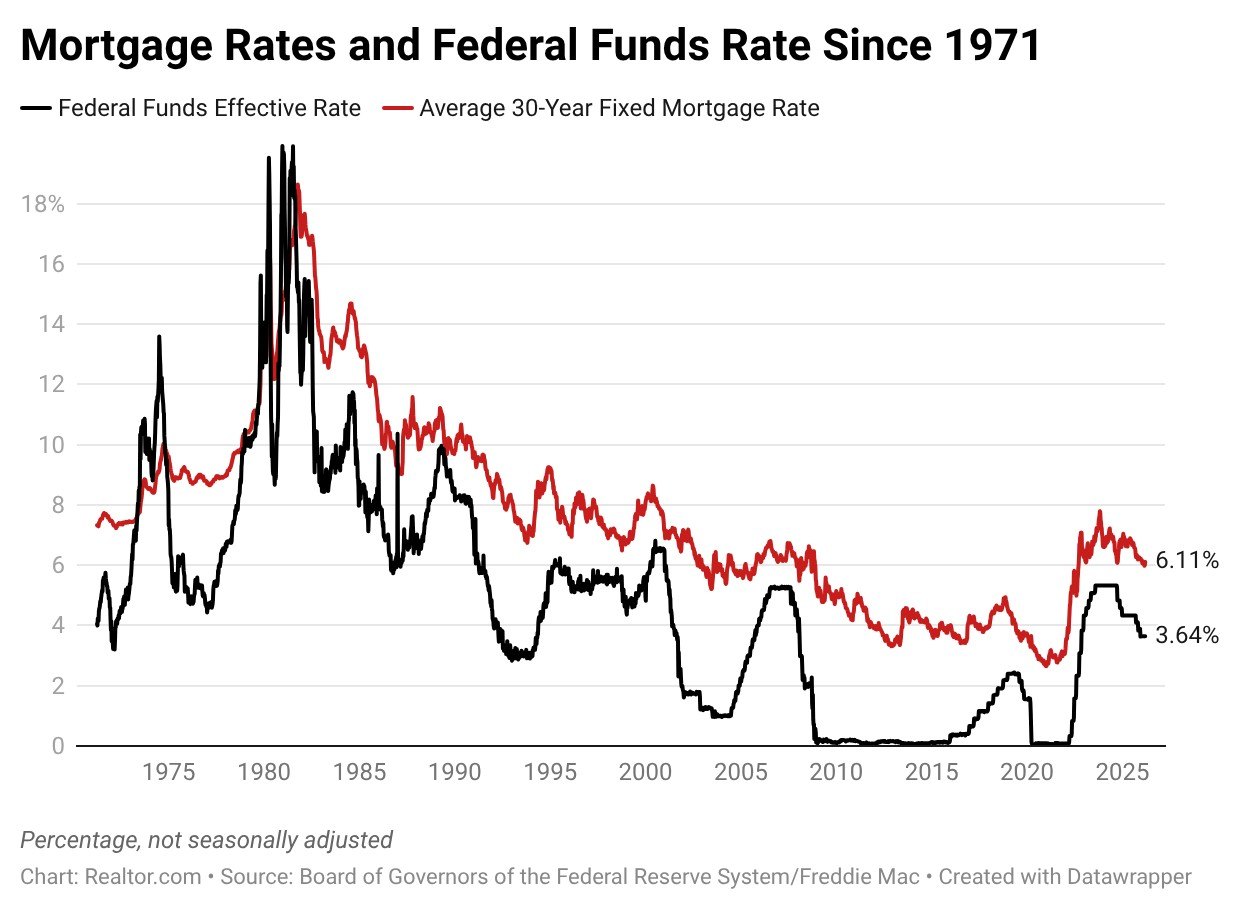

The decision leaves the Fed’s benchmark overnight rate unchanged in a range of 3.5% to 3.75%, where it has stood since December. After cutting rates three times last fall, the Fed paused at January’s meeting, and the outlook for future rate cuts is growing increasingly uncertain.

The Fed’s reluctance to cut rates has provoked the ire of President Donald Trump, who has demanded swift rate cuts since starting his second term. Trump reiterated the call on Wednesday morning, writing on his Truth Social site: “When is ‘Too Late’ Powell lowering INTEREST RATES?”

Mortgage rates, which touched a three-year low of 5.98% last month, have climbed steadily higher since the U.S.-Israeli war with Iran began on Feb. 28. Average mortgage rates reached 6.11% last week, according to Freddie Mac.

The upward trend in rates, driven by mounting fear of a global energy crisis, threatens to derail the crucial spring housing season, which had been shaping up to be promising for buyers before the war began.

“Mortgage rates are likely to move higher this week, but this won’t be in response to the Fed’s meeting,” says Realtor.com® Chief Economist Danielle Hale. “Rather, developments in the Middle East that are likely to spill over into inflation have been the biggest recent drivers.”

The Fed does not directly control mortgage rates. Rather, it sets the short-term interest rate for lending between commercial banks.

The central bank uses higher interest rates to fight inflation and lower rates to stimulate the job market, in line with the Fed’s dual mandate of price stability and maximum employment.

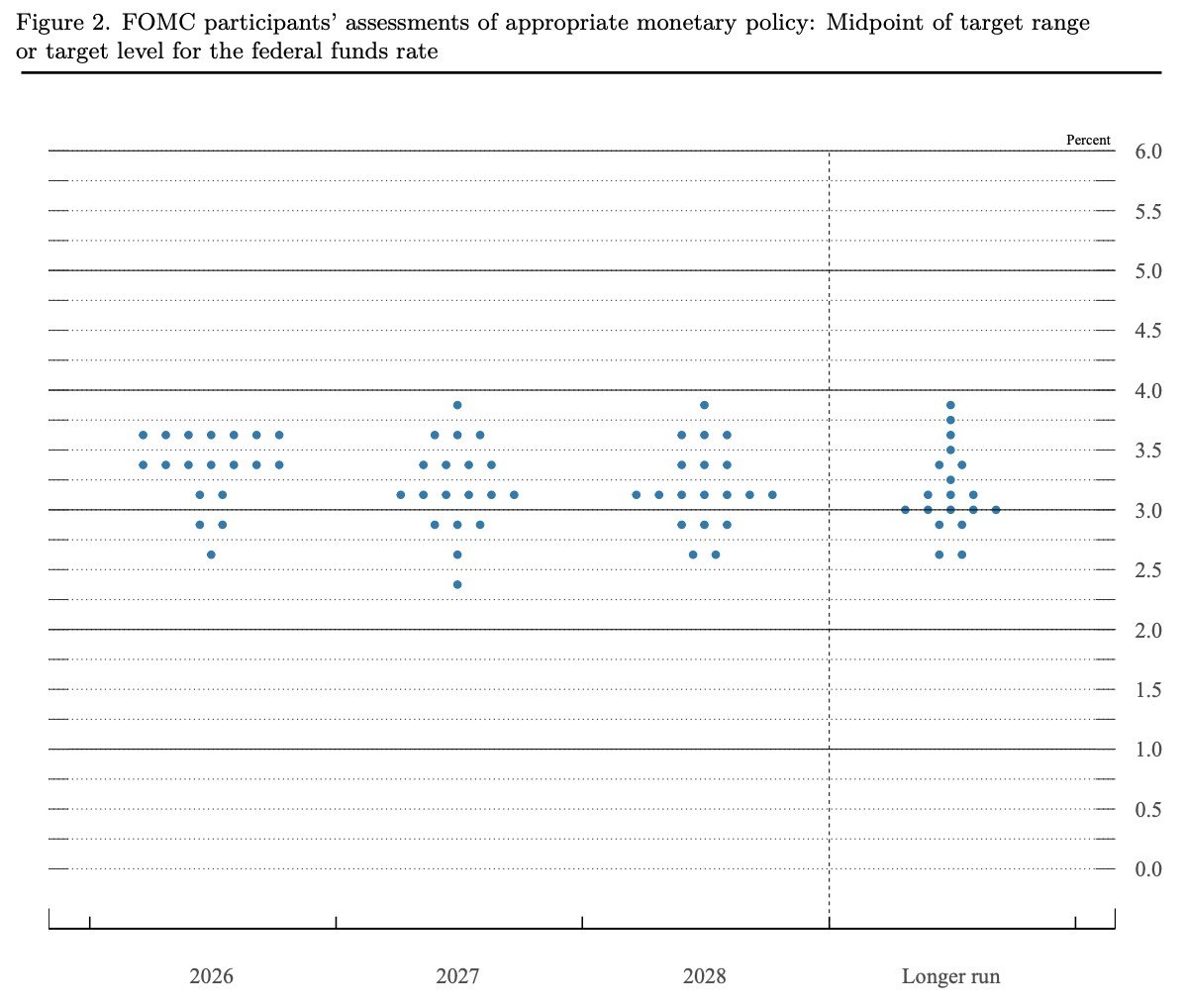

New projection shows little change in rate path

The FOMC released quarterly projections alongside Wednesday’s decision, offering a view into the expectations of committee members on the future path of interest rates.

The “dot plot” mapping member expectations for future interest rates showed little overall change from the last forecast issued in December.

Taking the median of the individual forecasts, the dot plot still calls for a single quarter-point rate cut in 2026, and one further rate cut next year. That’s unchanged from the December forecast.

“As is always the case, these individual forecasts are subject to uncertainty, and they are not a committee plan or decision,” said Powell. “Monetary policy is not our preset course, and we will make our decisions on a meeting-by-meeting basis.”

Despite the guidance, market expectations for a rate cut sometime in 2026 are diminishing.

Financial markets now assess a 48% chance that the Fed’s policy rate will be the same in December, up from just 33% a week ago, according to CME FedWatch.

On prediction marketplace Polymarket, traders rated a 27% probability of no rate cuts in 2026, up from around 18% a week ago.

Powell to remain on board until DOJ investigation concludes

In his remarks at a press conference following the vote, Powell confirmed that he will refuse to resign from the Fed’s board of governors until the Justice Department concludes its criminal investigation into his Senate testimony.

“On the question whether I will leave while the investigation is ongoing, I have no intention of leaving the board until the investigation is well and truly over with transparency and finality,” Powell said.

In January, Powell revealed that he had been targeted by a federal criminal investigation into his testimony about cost overruns in the Fed’s ongoing headquarters renovation.

Last week, a federal judge slammed the DOJ investigation as a blatant pressure tactic in Trump’s campaign to force Powell to either reduce interest rates or resign.

Powell’s term as Fed chair expires on May 15, but he has the option to remain on the board of governors as a regular voting member until January 2028.

Typically, Fed chairs resign from the board when their leadership term ends. But Trump’s pressure campaign for lower rates may change the calculus for Powell, who has been vocal in his defense of Fed independence from political pressure.

Powell said on Wednesday that he had not yet decided whether to step down from the board after the investigation concludes.

If Kevin Warsh, Trump’s nominee to replace him, is not confirmed by May 15, Powell says that by law he would continue to serve as acting Fed chair.

A key Republican senator has said that he will not allow any Fed nominations to move forward until the criminal investigation into Powell is concluded, calling the DOJ probe “weak and frivolous” and a threat to Fed independence.

What the Fed rate decision means for homebuyers

Bankrate financial analyst Stephen Kates says that with the Fed signaling restraint, homebuyers should expect mortgage rates to remain above 6% throughout the spring.

“Eager homebuyers should not anticipate fast-acting rate reductions that will pave the way for refinancing,” he says. “If you try to date the rate and marry the house, you could be setting yourself up for a difficult engagement.”

Eddie Garcia, CEO of national brokerage Realty of America, puts a more positive spin on the rate pause, saying that homebuyers should view it as a stabilizing move that reduces uncertainty.

“The last two years created hesitation across the market. It wasn’t just higher rates; it was the constant movement. Buyers and sellers didn’t know where things were going, so they paused,” Garcia tells Realtor.com. “When that uncertainty starts to settle, people step back in.”

Likewise, Michael Reisor, a real estate agent in Texas and New York and founder of Reisor.Team at Compass, predicts that 2026 will be the year that homebuyers move off the sidelines and stop trying to time interest rates.

“At this point, many clients realize waiting for the perfect moment is no longer realistic,” he says. “If buyers keep waiting for rates to fall, home prices may continue to rise in the meantime.”

Meanwhile, Garcia says that although he isn’t seeing any impact on housing demand yet from geopolitical tensions in the Middle East, a prolonged surge in oil prices could change that.

“That disproportionately impacts entry-level buyers,” he says. “As gas and everyday costs rise, disposable income shrinks, which directly affects how much buyers can afford on a monthly payment.”

While that wouldn’t crash the housing market, it would slow activity at the lower price points and make buyers more cautious, Garcia predicts.

“That said, the bigger issue is still supply. We don’t have enough homes, especially at affordable levels. Until that changes, demand will continue to hold up better than people expect, even with outside pressure,” he says.

Garcia says he often reminds clients that real estate is hyperlocal, and that what’s happening nationally doesn’t always affect a specific neighborhood or property.

“For sellers, that means pricing correctly from Day 1 based on real data,” he says. “For buyers, it means understanding where the opportunities are and how to compete strategically without overpaying.”

Developing story, more to follow.