Growing fears of a global energy crisis threaten to derail the crucial spring housing season as the U.S.-Israeli war with Iran sends oil prices soaring, with the path to a resolution unclear.

In the U.S., regular gasoline prices hit an average of $3.72 per gallon on Monday, up 27% from a month ago and the highest since October 2023, according to AAA.

President Donald Trump, who made lower gas prices a central vow of his campaign, has insisted that the price disruption will be a temporary blip that disappears quickly after a swift military victory over Iran.

But there are growing signs that Iran is intent on waging a prolonged war of attrition against the global economy by restricting tanker traffic through the Straight of Hormuz, a key passageway for 20% of the world’s crude oil supply.

On Sunday, Iranian Foreign Minister Abbas Araghchi appeared on CBS News’ Face the Nation, saying “nothing is on the table” in terms of a negotiated settlement, and insisting “we are ready to defend ourselves as long as it takes.”

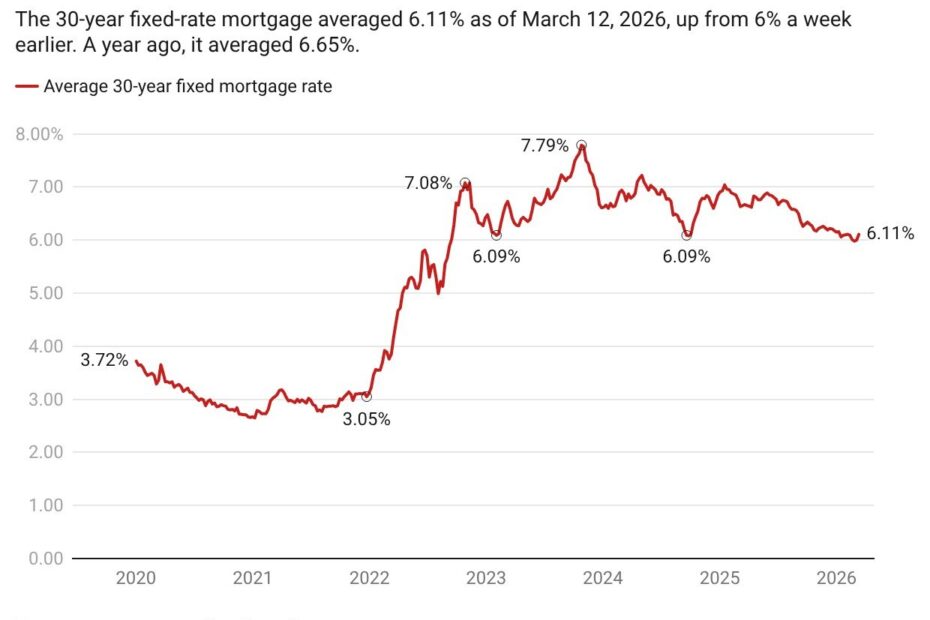

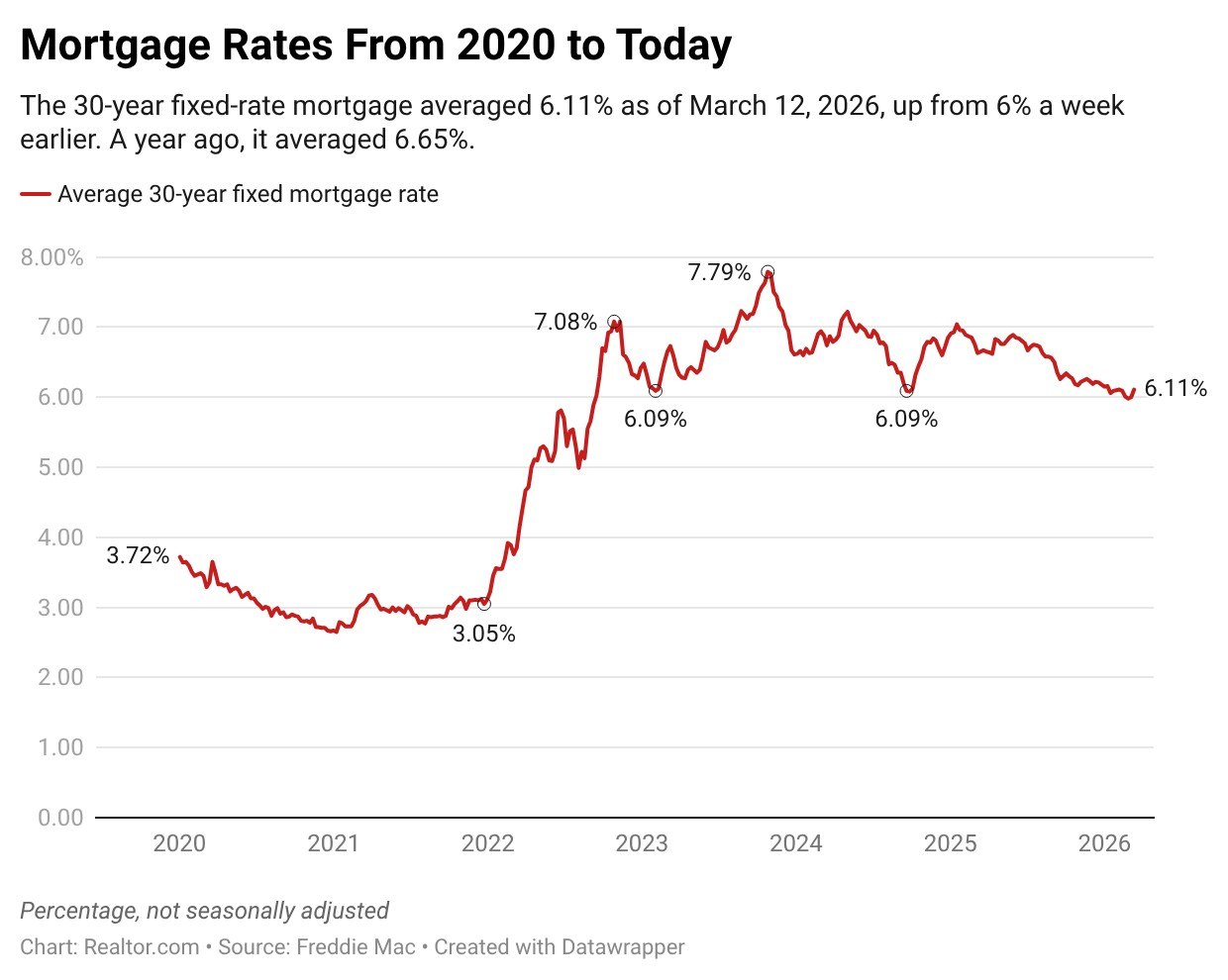

For the housing market, the war’s full impact is still unclear. But as the conflict enters a third week, it continues to send mortgage rates higher, just as the spring homebuying season kicks off.

“The biggest impact to the housing market of the war in Iran and subsequent oil shock will be through mortgage rates,” says Realtor.com® Senior Economist Joel Berner. “Wartime inflation is common generally, but the fears surrounding it for this conflict are especially pronounced because of the impact to global oil distribution.”

Brent crude oil, the international standard, has remained above $100 per barrel since last week, up from around $70 before the war began.

“The significant increases we have already seen to oil prices make their way into the cost of shipping every physical thing in the global economy, creating upward price pressures throughout,” says Berner. “When prices are expected to be higher in the future, tomorrow’s money is less valuable and today’s money gets more expensive, which is what we’re seeing with mortgages as rates continue to rebound from their low point at the end of February.”

Mortgage rates touched a three-year low of 5.98% in the final week of February but have since climbed sharply higher, hitting 6.11% last week, according to Freddie Mac.

Rates are expected to continue climbing this week, even with the Federal Reserve widely expected to make no change to the benchmark interest rate at its policy meeting this week, as renewed inflation fears cast doubt on the central bank’s ability to lower rates in the near future.

“Beyond rates, a prolonged oil shock will deteriorate already-weak homebuyer sentiment,” says Berner. “Before the war was initiated, things had been shaping up nicely for homebuyers this spring as prices were falling, inventory was rising, and mortgage rates had finally broken the 6% threshold.”

Despite those positive signs, existing home sales lagged in January and February compared with 2025, as lackluster consumer confidence continued to weigh on demand.

“Now, they’re even less confident, and as they feel the pinch at the pump and see prices rising across all sectors of the consumer economy, they’ll feel even less inclined to take on a new mortgage at a higher rate,” says Berner.

Although gasoline accounts for just 3%-4% of the typical household’s monthly budget, gas prices are a powerful inflation signal in part because they are trumpeted across roadside billboards.

As well, prolonged increases in gas prices ripple throughout the economy, as they raise transportation costs for groceries, clothing, and a wide range of consumer goods that ship by truck.

Eventually, homebuilders who are already struggling with high labor and materials costs may also feel the pinch.

“In the medium to long term, increased shipping costs will make their way to builders who have to pay more for materials, and those increased cost pressures will result in fewer homes being built and at higher prices,” says Berner.

Despite growing concerns about the war’s impact on homebuyers, mortgage applications to buy a home rose last week, according to the Mortgage Bankers Association’s weekly application survey.

Purchase applications were up 7.8% from one week earlier, on a seasonally adjusted basis, and rose 11% from the same week one year ago.

February data on pending home sales, a leading indicator for March closings, is due out on Tuesday and will provide another key signal about the strength of the spring housing market.