From rent affordability to mortgage rates and housing supply, here’s what’s changing—and what it signals for you and the year ahead.

We know rents are a challenge for many, and this month’s report showed just how much for some. A pair of minimum wage workers would find it affordable to rent a typical unit working a 40-hour week in just five of the 50 largest metro areas.

This is even as we saw more softening in the median rent price for a 28th straight month. The good news: As state and local minimum wages reset in some markets with the new calendar year, we expect two more markets—Jacksonville, FL, and Detroit, MI—to join this list.

Turning to broader macro trends, with the federal statistical apparatus back up and running, we got updates on both the labor market and inflation. We saw the unemployment rate tick up in November, as the private sector continued to add jobs, and the federal government continued to shrink its workforce. Earnings rose 3.5%, in line with recent trends.

Meanwhile, inflation readings improved. Core inflation, specifically, registered its lowest pace since March 2021.

These indicators are key measures of overall economic health and guideposts the Fed will use to evaluate the stance of monetary policy. While inflation remains above target, the direction of travel for both inflation and the labor market bolsters the case of those calling for cuts.

But others will argue that it takes time to see the effects of monetary policy on the economy, and the recent spate of reductions that moved the rate down through December could be sufficient. Market odds still favor this latter interpretation, suggesting that the Fed is likely to hold off on additional rate cuts in early 2026, keeping mortgage rates relatively steady in anticipation.

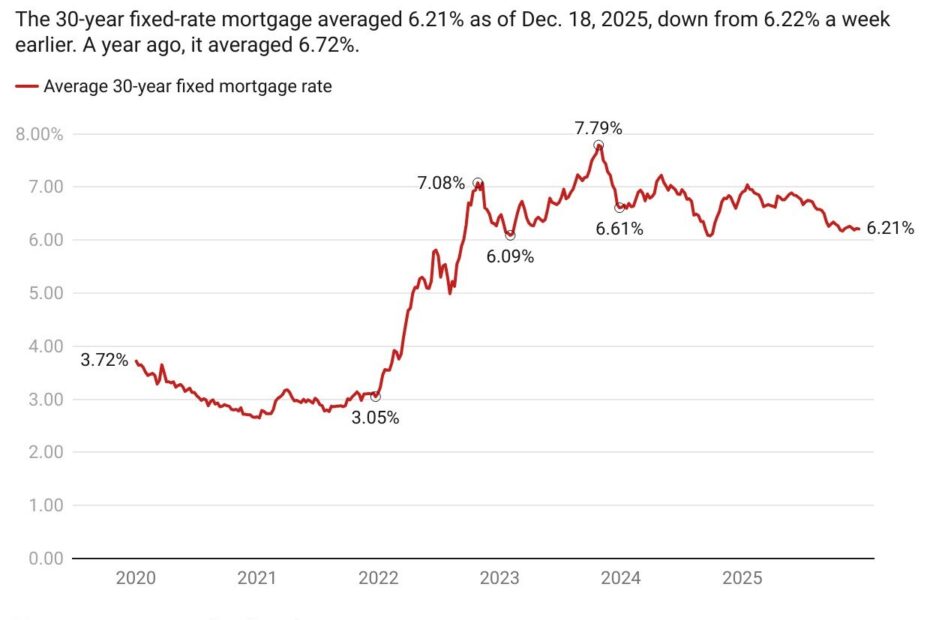

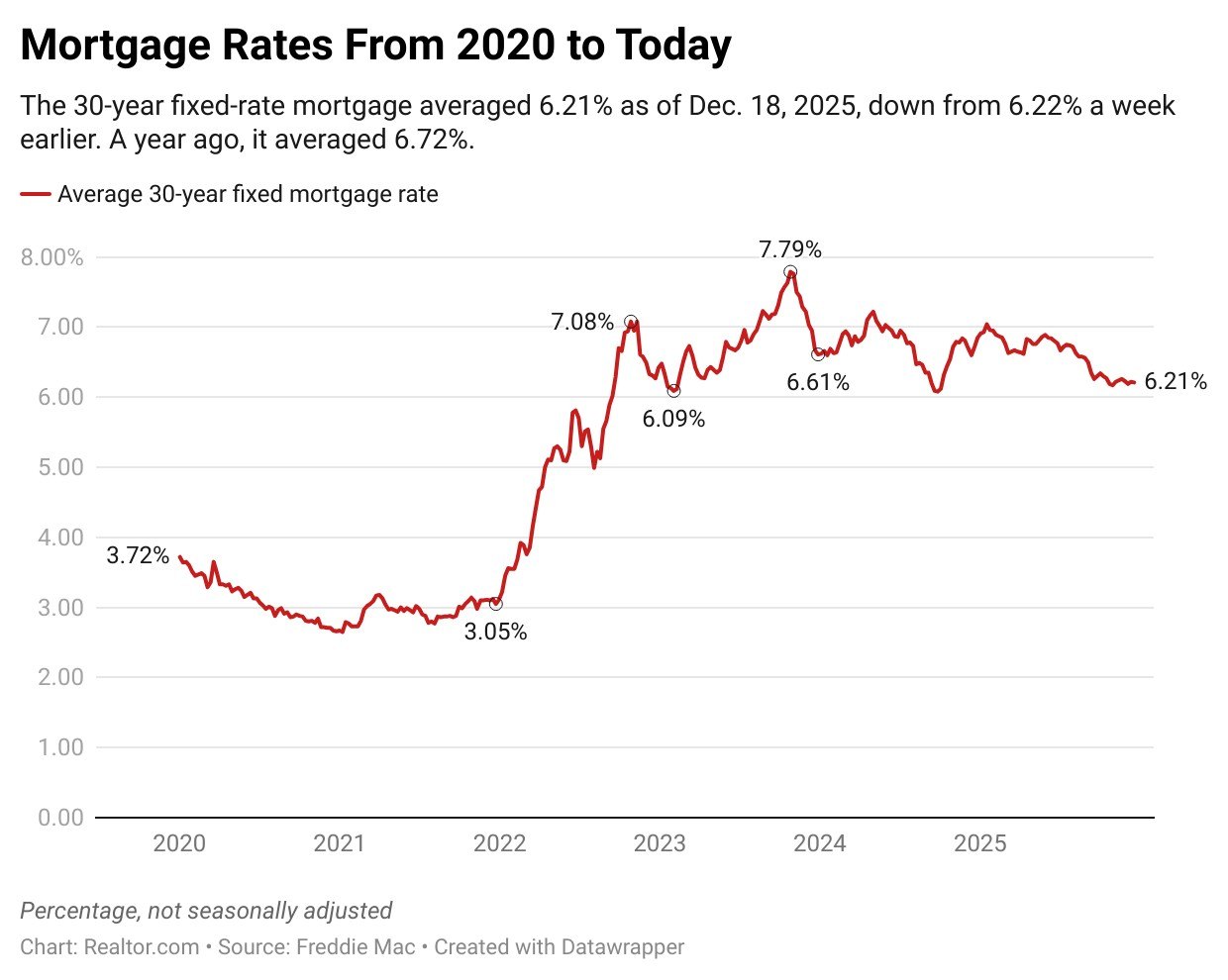

Even before this data, mortgage rates were essentially unchanged, dropping just 1 basis point this week. This steadiness has made it easier for homebuyers to budget, and fortunately for those homebuying as a New Year’s resolution, the Realtor.com® housing forecast anticipates mortgage rates to continue roughly as they are through 2026.

Weekly trends in housing data have been very similar to prior weeks. One noteworthy departure is in the trend for newly listed homes, which was nearly flat in the week, an improvement over recent larger declines that will improve options for buyers.

Existing home sales in November rose in the month despite falling short of the year-ago pace as lower mortgage rates and more modest home price growth helped buyer incomes stretch further.

Looking at the types of homes on the market, we see that buyers often prefer move-in ready homes, and “flipped homes”—older homes that have been purchased to renovate and resell—often fit this bill.

However, with financing costs still quite high, the luster of flipped homes has faded. Their views-advantage has waned compared to 2021, and flipped homes sold for larger discounts relative to asking than other older homes. If you’re shopping for flipped homes, you may be able to negotiate; and if you’re selling a flipped home, be sure to calibrate your pricing.

You’ve heard me speak often this year about the supply challenge facing the housing market and the opportunity areas where we’re building more homes as part of our Let America Build campaign. I recently joined the National Housing Supply Summit 2025 Year in Review webinar with several other experts to highlight the progress and challenges that remain.

And for those of you dreaming of ski season and luxurious mountain estates, our luxury spotlight features trends in Heber, Utah, an outdoor paradise where the luxury tier starts at roughly six times the national luxury price point.