Although the spring selling season is typically characterized by bustling energy, both buyers and sellers are pausing and readjusting their financial expectations this year as a significant jump in mortgage rates hit the market last month, compounding with skyrocketing gas prices and continual pressure from the insurance side.

This industry-wide pressure has developed into a state of underinsurance, driven by inflated construction costs, reduced insurance protection, and limited coverage options. And one of the root causes is what the Senate Budget Committee deemed a “looming economic threat”: the climate crisis.

Natural disasters increase the cost of insurance around the country as insurers pay out billions of dollars following high-scale losses—all in an economy where people are already cutting costs and struggling to afford both their premiums and their deductibles.

Plus, some insurers are actively withdrawing from weather-adverse areas, drastically shifting the market and leaving many homeowners with fewer options and insufficient coverage.

Gaps from all angles

Underinsurance is increasingly a reality in today’s industry. A study from the University of Colorado discovered that almost 75% of homeowners lacked sufficient coverage for their wildfire claims, with over one-third falling into the “severely underinsured” category.

If you bought your policy six or seven years ago, explains John Meek, chief marketing officer of HUB International’s Private Client division, there’s a good chance that the inflationary factor has widely surpassed the replacement cost calculated at purchase.

“With what’s happened externally in the market with the rise of labor costs, material costs, and so forth, sometimes that inflationary increase doesn’t catch up fast enough,” he says.

Many home insurance policies automatically adjust the coverage limits at renewal to help account for these changes, but this feature is often unreliable during periods of rapid inflation.

“Even homeowners with inflation guard coverage can still face a shortfall if their policy limits haven’t been proactively updated,” says Lauren Menuey, Goosehead Insurance managing director.

While rebuilding costs are certainly creating their own environment of underinsurance, some homeowners find themselves stranded as insurers exit high-risk locations. They must explore specialty solutions that often require them to sacrifice coverage—a type of force-placed underinsurance.

“They’re going to take a policy that only gives them up to $2.5 million of coverage, even though they may have a home that’s worth $5 million. But because they can’t find anything else, they’re willing to at least take the $2.5 million. Something is better than nothing,” Meek explains.

Being underinsured is one thing—lacking coverage is completely another. Some perils simply aren’t covered by standard home insurance, like floods and earthquakes. Coverage for rebuilding to modern-day codes is also typically limited or excluded.

These risks require separate coverage, but most homeowners are hesitant to take on additional premiums when they’re already struggling to make ends meet. Even if they choose to address these gaps, they may remain underinsured. Maximum flood insurance limits are outdated by 20 years, and ordinance or law coverage, which helps with building code requirements, is typically set at 10% of your home’s dwelling coverage, although some insurers offer higher limits.

A costly error

There’s not only a gap in insurance protection but a gap in understanding. Nearly 40% of homeowners don’t know how to determine the appropriate level of coverage for completely rebuilding their homes, according to a 2025 survey conducted by Kin Insurance. Many assume their home’s replacement cost should mirror its real estate value.

This knowledge gap can be costly. When your coverage limits are too low, your out-of-pocket claim expenses increase. Any uncovered costs fall to you.

Underinsurance can also trigger what are called “co-insurance penalties,” which further increase your own financial responsibility. Many home insurance policies have a built-in “80% rule.” According to this condition, the policyholder must maintain a dwelling coverage limit of at least 80% of their home’s replacement value. Otherwise, a penalty is applied toward future claim payouts.

For example, say you are only insured to 75% of the required amount. A $100,000 claim payment would be reduced to $75,000, leaving you responsible for the remaining $25,000—in addition to your deductible.

Underinsured homes are less likely to be rebuilt when damaged and more likely to be sold, according to the University of Colorado. As a result, property values plummet and local economies suffer, especially in communities with higher climate risk and insurance accessibility challenges.

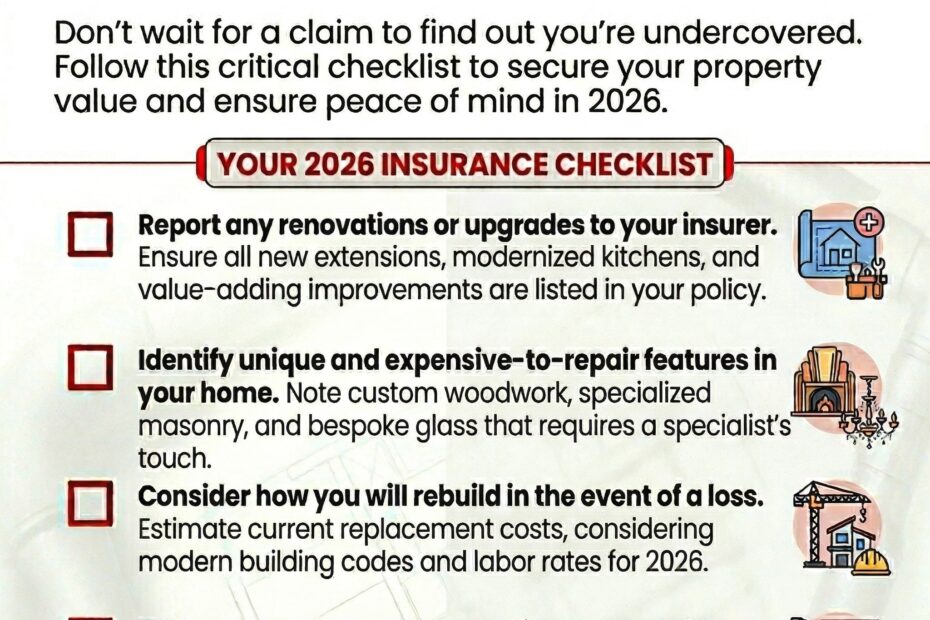

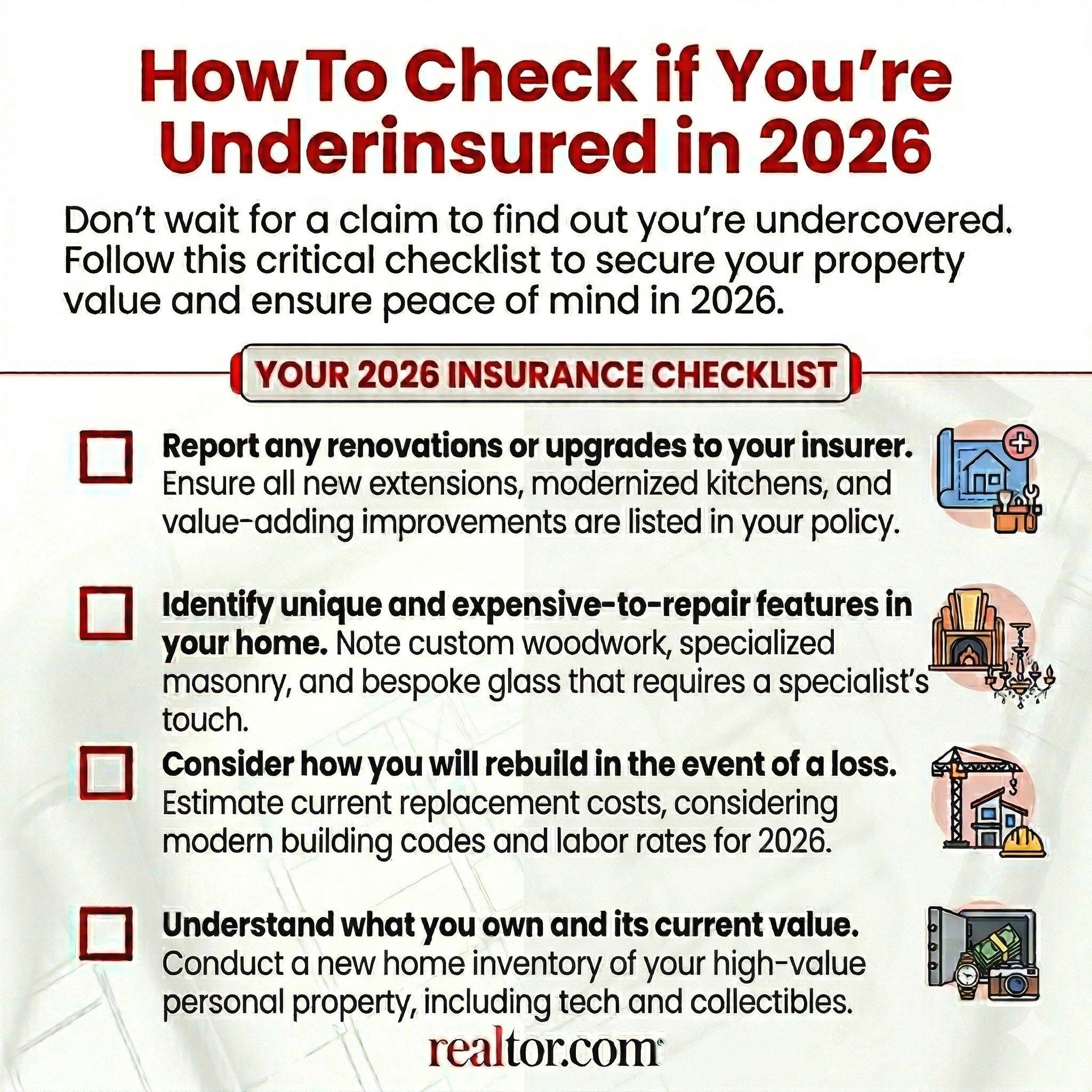

How to check if you’re underinsured in 2026, according to an expert

Working with an insurance agent or broker is often the best way to evaluate your coverage levels and adjust for changes in rebuilding costs. But as we’ve already seen, many homeowners don’t know where to begin, which means they likely don’t know which questions to ask or what actions to take.

To guide you along the way, Meek offers the following checklist.

Report any renovations or upgrades

“If you’ve done any type of renovating to the home, make sure that is a priority in your conversation with your broker or agent,” Meek says.

From bathroom and kitchen renovations to HVAC and smart home tech upgrades, failing to report these home improvements puts your investment at risk.

When calculating your home’s replacement cost, “[insurers are] going to defer to [what’s most] common, which is a builder’s grade or an average grade bathroom. And therefore, that Italian tile floor that you may have chosen for your bathroom isn’t going to be considered,” explains Meek.

He also reminds homeowners to provide documentation regarding pricing, materials, and labor and to consider major changes to contents, such as upgrading to high-end appliances during a kitchen renovation.

Identify unique and expensive-to-repair features

“You want to make sure you point out features in the home to your agent or broker that are unique [or] important to you, so we can have a dialogue about whether or not we have to accommodate that in the replacement cost,” Meek says.

He adds that this is especially important if you own an older home with expensive-to-repair, hard-to-replace characteristics that you wish to preserve.

Consider how you will rebuild in the event of a loss

Meek encourages homeowners to consider how they will repair or rebuild their home following a loss. Will you hire your own labor and source the materials? Or will you rely on your insurance company’s guidance?

“All of those things do impact the amount of time it takes to rebuild or renovate a home post a loss. And that also should be factored into the replacement cost,” he says.

Understand what you own

“Contents tend to get lost in this conversation of assessing how much you have and picking the right coverage,” says Meek.

He shares that it’s easy for homeowners to underestimate the value of their belongings by 40% to 60%, especially when they are unaware of what they own and what their buying habits are.

Clothes are the perfect example. Your outfits on current rotation are likely at the forefront of your mind, but do you truly know how much it will cost to replace them today? What about all the pieces hanging in the back of your closet?

“If you’re underestimating the stuff that you wear on a daily basis, you can only imagine what you don’t think about [and] what you take for granted,” Meek explains.

This is why so many in the insurance industry emphasize maintaining an up-to-date, detailed home inventory.

“Take those pictures of each room in the home, and make sure you’re also taking pictures of things that are special to you and that you felt you invested hard-earned money into,” he advises.

Similar to how insurers will defer to using builder’s grade materials when determining your home’s structural replacement cost, they will assume your items can be replaced with standard ones, even if you spent thousands on custom-made furniture, for example. And if you have actual cash value coverage, depreciation will further reduce your claim payouts.

“You don’t [want to] get yourself caught in that gap,” Meek warns.