More than 1.7 million homes in Chicago are at risk of moderate or severe hail damage, representing more than $1 trillion in reconstruction cost value (RCV), according to a new report.

It’s a striking figure for a city not typically thought of as one of the country’s major hail markets. The findings land just as forecasters warn the area could see severe thunderstorms on Thursday, including hail up to 2 inches in diameter.

The brewing storm neatly underlines the broader warning in the Severe Convective Storm Risk Report from Cotality, a data analytics firm.

Severe convective storms like hail, high winds, and tornadoes were once treated as a secondary concern for homeowners and insurers. But they are increasingly acting like a primary threat—one that is putting growing pressure on the insurance system meant to help communities rebuild.

From secondary to primary risk

Severe convective storms have long been overshadowed by the more visible destruction of hurricanes and wildfires. But as these storms become both more frequent and more expensive to recover from, that’s starting to change.

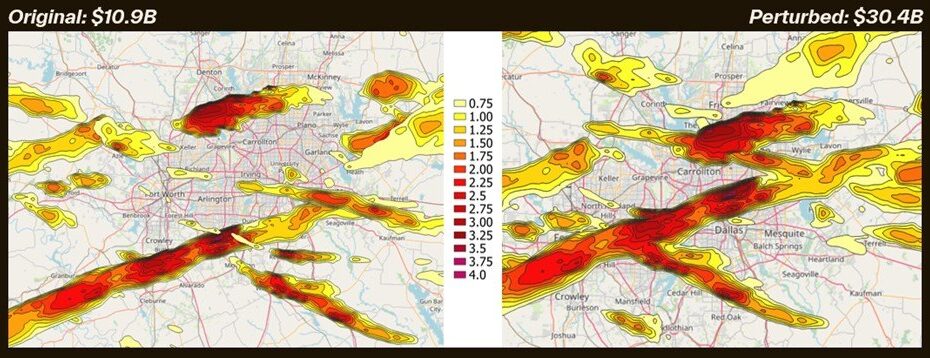

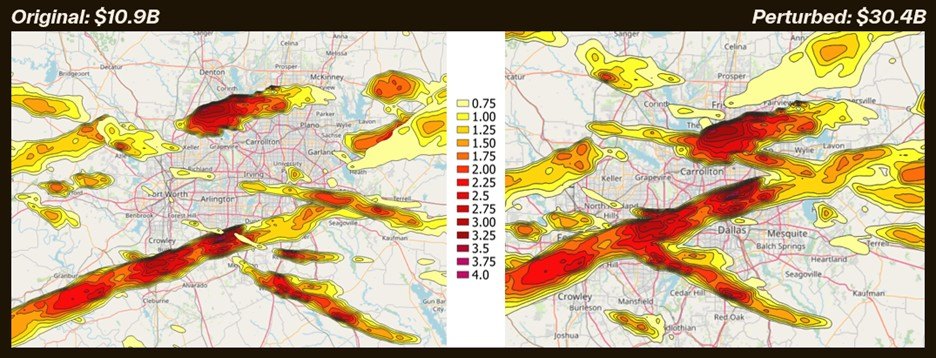

Hail is a big reason why. It now ranks as a major driver of property insurance claims, racking up major costs to insurers. In June 2023, for example, a storm cluster in Texas affected more than 680,000 homes and caused an estimated $7 billion to $10 billion in insured losses, according to the report.

These events are getting more frequent, too. In 2025, Cotality tracked 142 days with hailstones measuring 2 inches or greater, above the 20-year average of 122 days.

That poses a growing problem for an insurance industry already under pressure from the rising cost of flood and wildfire damage. It is now also being forced to reckon with hail, whose financial impact can rival the losses more commonly associated with major hurricanes.

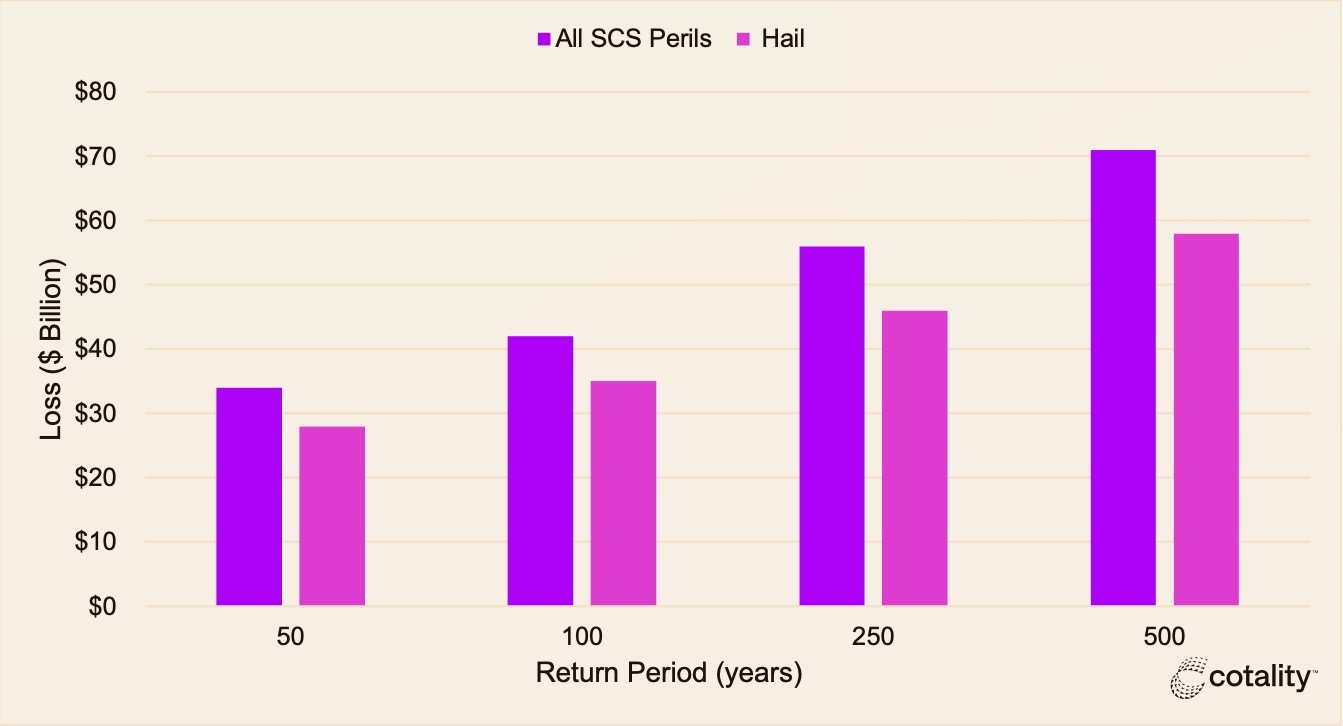

In its most extreme modeled scenario, Cotality found that a severe hailstorm could cause as much as $58 billion in losses. For perspective, that’s roughly the equivalent of insured losses caused by Hurricane Ian. Even less severe events could still generate nearly $30 billion in insured losses—roughly on par with Hurricane Sandy.

What the ‘Chicago anomaly’ represents

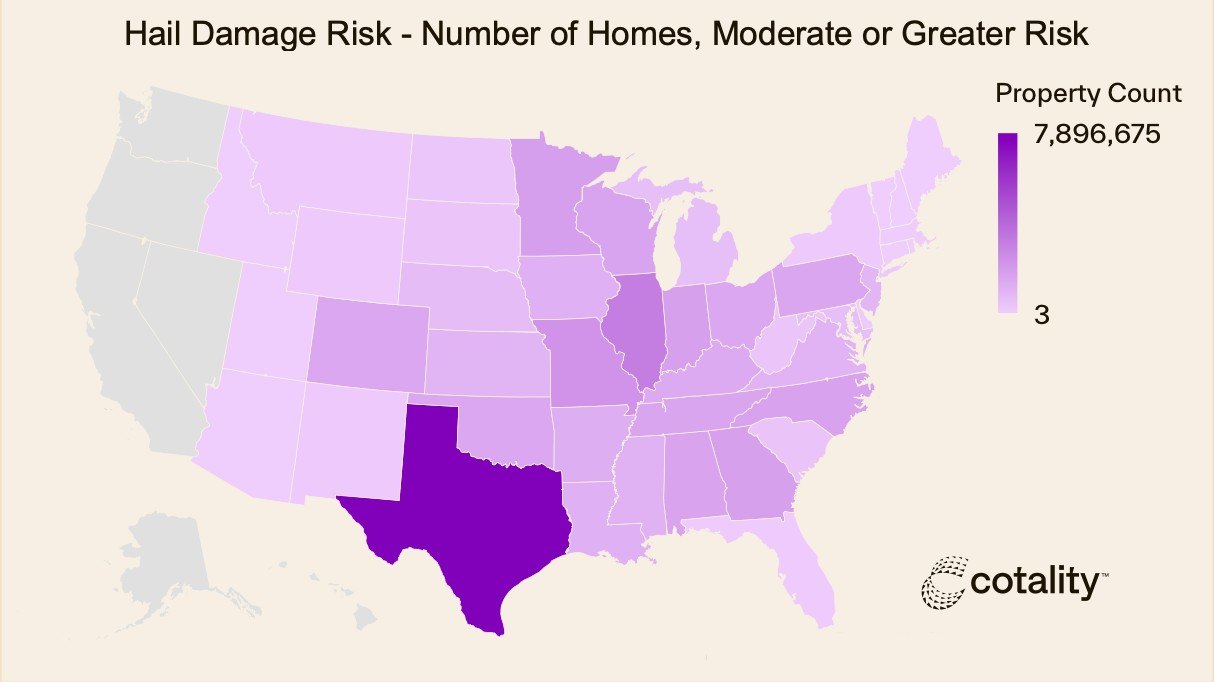

While hurricanes are confined to the coasts, severe convective storms affect a much wider swath of the country. More than 43.5 million properties fall into moderate or greater hail-risk categories nationally, representing a combined $17.8 trillion in RCV.

Texas leads the country overall, with nearly 8 million homes and $3.1 trillion in exposed RCV. But Illinois ranks second, with $1.5 trillion—almost all of which is concentrated in Chicago.

That’s what the report calls the “Chicago anomaly.” While Illinois is not typically thought of as a major hail state, its mix of moderate risk and high-density, high-value housing creates outsized cost exposure.

And it’s that mix that offers a prescient warning for the rest of the country: A market doesn’t need to sit in the nation’s most notorious storm corridor to face enormous financial risk.

What a severe convective storm does to a home

What makes these storms so damaging is that they can hit many parts of a home at once.

Hailstones that are 2 inches or larger can break windows, crack siding, and damage roofing systems. Once the home’s outer shell is compromised, water can penetrate and the damage can spread.

While it might cost $12,500 to repair a roof after a hailstorm, just one inch of water damage can cause $25,000 in repair costs, according to FEMA estimates. So what starts as seemingly straightforward and visible storm damage can quickly become a complex and expensive recovery.

That cascading damage is also what makes these storms so costly for the insurance industry—and they’re starting to take notice.

Last summer, one major insurer raised home insurance rates in Illinois by 27.2%—adding roughly $746 to the average policyholder’s annual premium. Another raised rates by 14.3%, following back-to-back increases of 12.7%.

They framed the hikes as simple arithmetic: For every $1 collected from Illinois homeowners in 2024, the company says it paid out $1.26 in claims and costs. In 2023, that number was even higher: $1.30 per $1 collected.

The biggest culprit? Hail. The company reported $638 million in hail damage claims in Illinois in 2024, second only to Texas, which topped $1 billion.

The real homeowner consequence: Cost, claims, and delay

Cotality frames recovery after these storms as a fragile, multistep chain that depends on underwriters, catastrophe modelers, claims teams, and restoration contractors all functioning in sync. When any part of that chain slows down, the timeline and cost of recovery can grow exponentially.

The report illustrates that risk with a hypothetical scenario: A three-week claims delay allows repeated rain intrusion, turning a roof problem into a mold-driven gut renovation, driving costs far beyond the original repair and displacing the family for months.

It may be a fictional example, but it reflects a reality more homeowners may have to contend with. And that could mean shouldering higher home insurance costs, even as the path from damage to repair grows more complex and less predictable.