More than 1.45 million acres across the Western U.S. have already been ravaged by wildfires in 2026, and multiple states are now bracing for what could be one of the country’s most devastating fire seasons.

After one of the warmest winters on record in the U.S., experts are warning that a low snowpack and a searing heatwave in the West are already boding ill for the months to come.

In January, the National Interagency Fire Center (NIFC)—the federal body tasked with forecasting wildfire risk—predicted an “above-normal” season for much of the country. Today, an early start to those flames is acting like a grim exclamation point on that prescient warning.

Nebraska is currently battling the historic Cottonwood and Morrill fires, two events that have already scorched more than 780,000 acres combined. The events also mark the state’s worst fire season on record—just three months into the year.

In nearby South Dakota and Wyoming, firefighters are battling smaller blazes against high, dry winds that threaten to make them out of control. And across the country, more than 1.45 million acres have already burned this year, according to the NIFC—and it’s only March.

Wildfire experts are warning these patterns are the beginning of a fundamental collapse of the traditional fire season calendar—something that could pose a serious risk to homeowners who find themselves caught between an insurance industry in crisis and expansion into wildfire urban interface areas that face some of the highest fire risks.

A perfect storm

In March 2026, the Western U.S. hit its lowest snowpack levels in 40 years. Across Arizona, New Mexico, and Nevada, snow-water levels are sitting at less than 50% of normal, according to the National Integrated Drought Information System.

That poses both a serious threat to the water supply of these states as well as the loss of the spring buffer that usually keeps fuels too wet to burn until July.

March has also seen temperatures 20 to 40 degrees above average across the Southwest and High Plains. By late in the month, high-temperature records had already been broken in at least 14 states.

Temperatures that high risk baking the moisture out of soil and dormant vegetation, turning it into fuel that can easily catch fire from a lightning strike or human-caused spark.

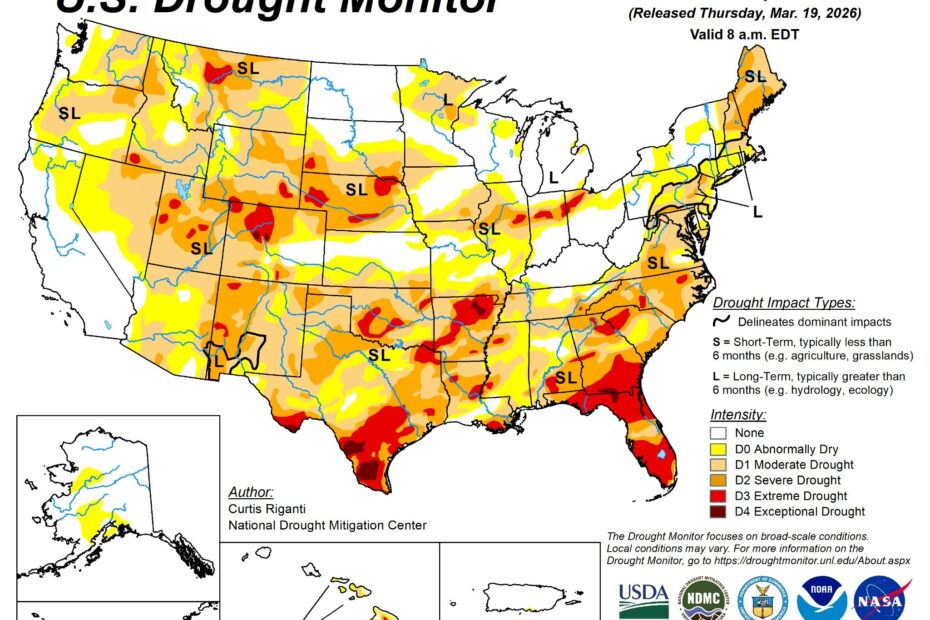

Risk isn’t just contained in Western states, either. The U.S. Drought Monitor currently classifies over half the country as “abnormally” to “moderately” dry.

All of these factors are cited in the NIFC’s updated forecast for the 2026 fire season, which it sees as normal in much of the country, with the highest risk concentrated in the South. Even so, NIFC puts the national preparedness level at 2 out of 5: a level that reflects increasing risk against underlying stability.

But River Selby, a former hot shot—the most elite and highly trained type of wildland firefighter—wrote in a recent Substack post: “I am suspicious of these claims of ‘low levels’ and ‘modestly increasing’ fire activity.

“That’s clearly untrue given the high regional preparedness level and the absolutely bonkers 422% February increase of the previous 10-year-average, which accounts for February 2024.”

Selby, who uses they/them pronouns, is referencing an NIFC report that showed a more than 400% increase in the acreage that has already been burned across the country. Their warning is that we’re using an old map for new territory. For homeowners, that may mean rewriting the book on what a fire-hardened home looks like.

Up against an industry in trouble

Homeowners need to understand their risk as the new fire season collides with an insurance industry in crisis.

Between 2018 and 2024, some 1.9 million home insurance contracts were dropped nationwide, according to an investigative report from the Senate Budget Committee. Areas facing greater fire risk had higher nonrenewal rates than those in low- or moderate-risk areas.

As private insurers flee high-risk areas, homeowners have been forced into state-backed last-resort plans that offer less protection, often for higher costs. For those who live in these areas, that means navigating a volatile market to protect what is often their most valuable asset.

The growth of California’s FAIR plan is an apt example. As of December 2025, the total exposure of the plan is $726 billion—a 4% increase from the previous fiscal year and a 230% increase since the 2022 fiscal year.

That’s a lot of exposure for a plan that was never meant to be a first-line defense, and there are questions about whether these plans can handle their growing policy load.

The fallout from the 2025 Los Angeles fires already exposed these limits. The fires erased an estimated $8.3 billion in home value across the city, according to research from Realtor.com®.

“Taken together, the sales and valuation data indicate that the fires led to large, immediate losses in housing wealth for destroyed properties, alongside more moderate but widespread value softening across surrounding neighborhoods,” explains Realtor.com senior economic research analyst Hannah Jones.

For some, recovery was made more complicated by a convoluted claims system. A subsequent investigation into the FAIR plan’s response revealed systemic problems that left wildfire survivors with delays, denials, and inconsistent claims decisions.

Today, 7 in 10 L.A. fire survivors have yet to return home—at least in part due to insurance difficulties, according to a survey released by the Department of Angeles, a nonprofit group formed after the fires.

The historic WUI expansion

The financial instability of the insurance industry is being compounded by the rapid, historic expansion of the Wildland-Urban Interface (WUI). Nearly one-third of homes in the continental U.S. are now located in these zones. According to U.S. Forest Service research, this footprint expanded by 179,000 square kilometers between 1990 and 2020—an area roughly the size of Washington state.

This expansion isn’t just a matter of geography; it is an escalation of danger. Homes in these areas face three times the risk of destruction compared to two decades ago, according to a 2025 study from the University of Wisconsin-Madison. With more than 1,100 communities now vulnerable to urban wildfires on a scale comparable to the 2025 L.A. fires, millions of homeowners are finding themselves squarely in the line of fire.

As record heat and vanishing snowpacks turn the U.S. landscape into a powder keg, living on the edge of nature now requires navigating a broken insurance system where the financial safety net is as fragile as the dry timber surrounding it.