Single women outpace single men in homebuying nationwide, asserting their force in the market despite widespread affordability pressures that have discouraged many other segments of buyers.

“They truly are this tremendous force,” said Jessica Lautz, the deputy chief economist and vice president of research at the National Association of Realtors, during a panel discussion at the Realtor.com® 2026 SXSW Open House.

“If we look across all generations of homebuyers, what we see is that single women are always outpacing single men, and they’re always second only to married couples in the housing market,” she added.

That trend has helped female homeownership hit an all-time high of over 20 million homeowners, according to a report from First American Financial Corp.

These milestones are especially striking given that women still earn just 85 cents for every dollar men make—and that, until the 1974 Equal Credit Opportunity Act, they could be legally denied a mortgage based solely on their sex.

The resilience and dominance of this segment of buyers offers lessons for the market as a whole, proving that even in a high-interest-rate environment, the desire for equity and stability can outweigh significant affordability hurdles.

A transformation, not a trend

“This isn’t just a market trend conversation today. This is really about cultural transformation,” Anna Marie Castiglioni, Head of Realtor.com Next, said in the wide-ranging discussion.

At the core of that transformation, is more women stepping into their power, Sheryl Palmer, CEO, Taylor Morrison, the fifth-largest homebuilder argued.

“If we go back 10, 15, even 20 years, the female was known as the veto in the purchase decision. Today, they’re actually a decision maker,” she said, noting that women now account for 40% to 45% of all Taylor Morrison’s mortgage leads.

It mirrors the story of Sindhu Nair, a digital product manager who bought her first home at 46 years old.

After losing a house on closing day in 2021, she left the market, only to have a moment of clarity four years later.

“I would pay my landlord through Cash App,” she told Realtor.com in a recent profile on generational wealth. “I saw how much I was paying in rent, and decided, ‘No, that’s money that I could have been putting towards a house.’”

In late 2025, Nair closed on a $325,000 row house in the Port Richmond neighborhood of Philadelphia, and began her journey building equity instead of paying rent indefinitely.

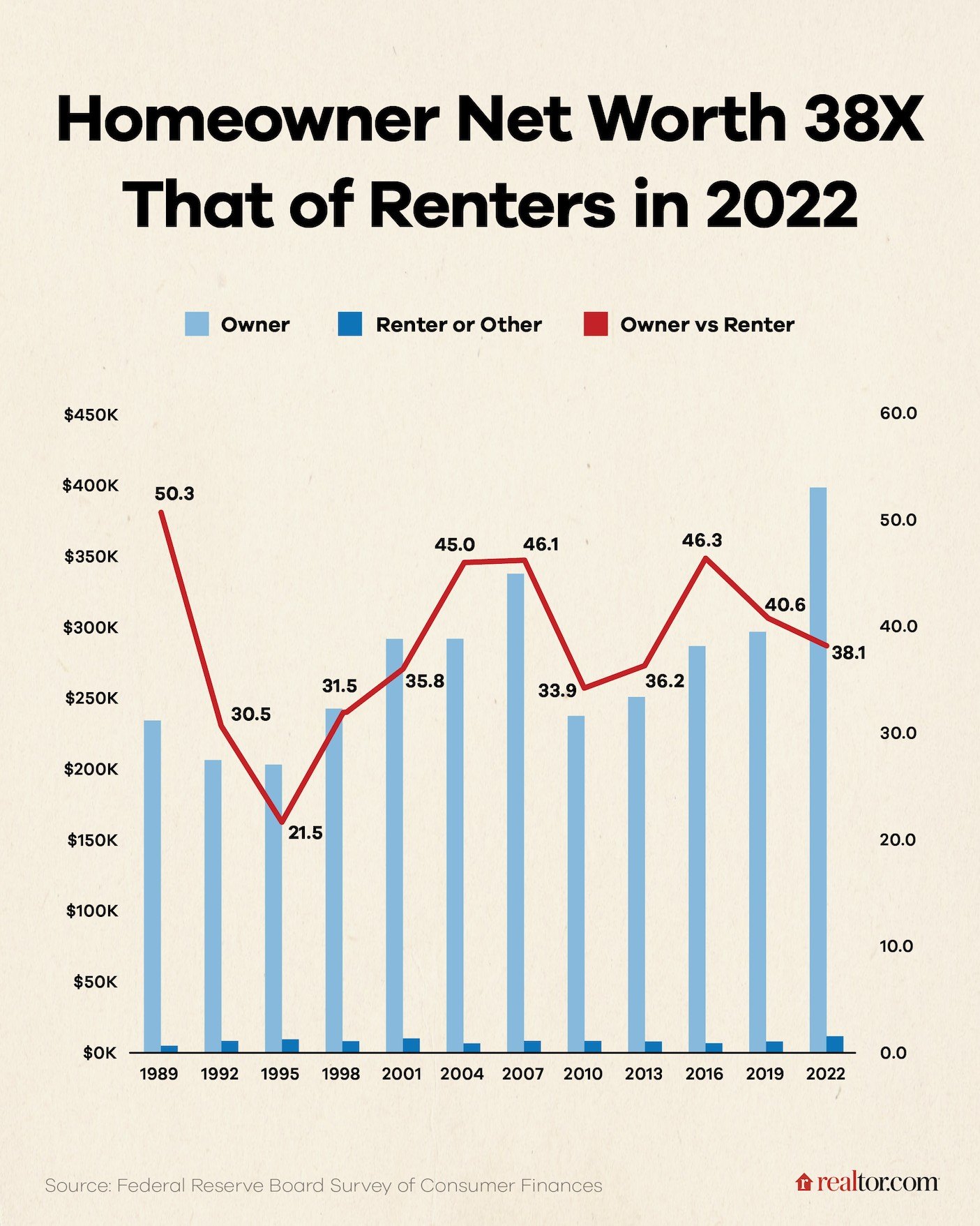

That decision can have an outsized impact on her net worth: Homeowners have approximately 38 times the net worth of renters, according to the Federal Reserve’s Survey of Consumer Finances.

‘Equity is such a magical thing’

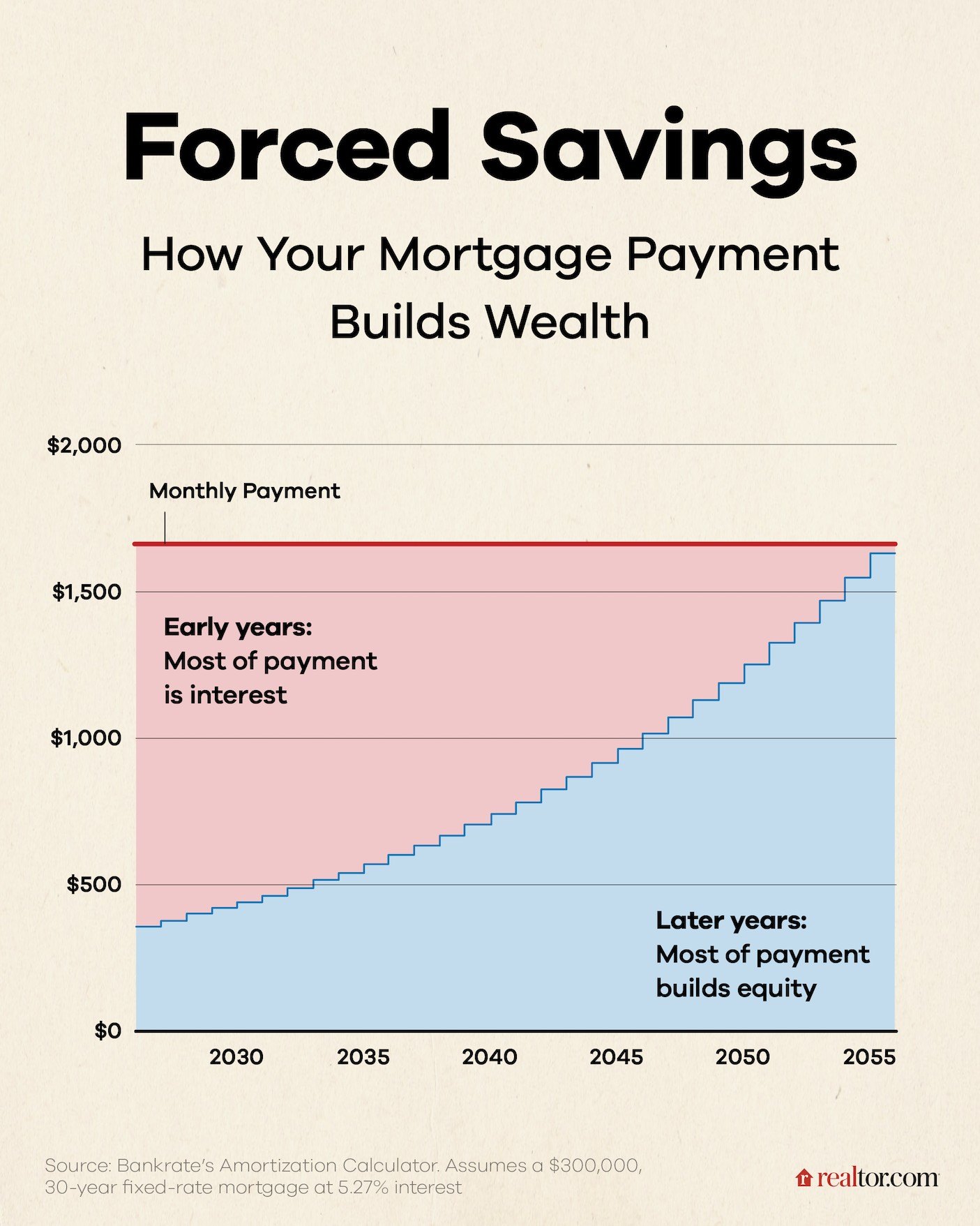

Behind that net worth gap is the power of equity.

“Equity is such a magical thing that we don’t talk about enough,” said Lindsey Stanberry, founder and CEO of The Purse, a publication that focuses on personal finance and lifestyle topics important to women.

As you pay down your mortgage, more of your monthly payment goes towards paying of your principal balance and building your equity. Your home is also likely to become more valuable over that time period, too—super-charging your equity.

But timing is an important aspect in that equity building power.

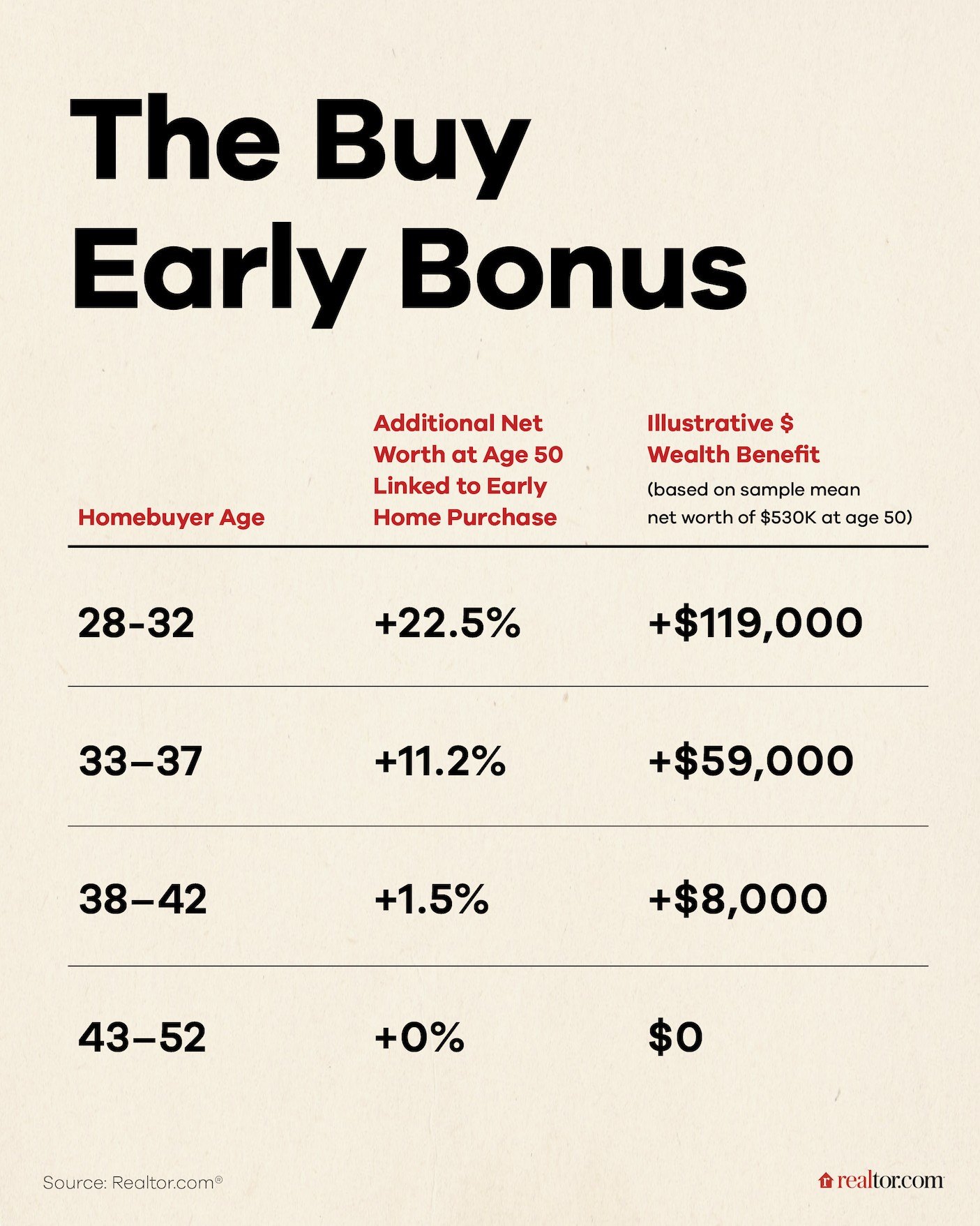

New research from Realtor.com shows that purchasing your first home by age 32 can result in a 22.5% or $119,000 higher net worth by age 50 than waiting just 10 more years to buy later.

And yet, the median age of first-time single women buyers is 44—five years older than the median age of first-time male buyers, according to data from the National Association of Realtors. That difference that can translate into a muted mid-life net worth boost.

‘Don’t gatekeep’

When asked what could be done to get more women into the market and earlier, Lautz had a simple answer: “Don’t gatekeep.”

“Talk about your pathway into homeownership and have those other conversations. Skip brunch, have everyone over to your new house, and then tell everyone how you got there,” she said.

In addition to financial education, the panel also highlighted low down payment options like VA and FHA loans as vehicles to enter the market. These programs can be particularly powerful for single female buyers because saving on one income can extend the timeline to save for a down payment—which already takes the typical first time buyer 10 years, according to research from Realtor.com.

“I was just talking to a young woman and speak who qualified for a very low down payment on her salary, she was a lawyer, and such a game changer for her,” added Stanberry. “Just finding out about those like the needle and an impact for many people.”

New construction also got a shoutout from panelists for offering low maintenance homes, often with steep discounts like rate buy downs or offers to cover the cost of private mortgage insurance (PMI) for a fixed set of years.

Stanberry offered one last piece of advice: “This is totally doable,” she said. “Homeownership in the U.S. isn’t for everyone, but if it’s for you, go for it.”