The federal government shut down this week for the first time in more than seven years. That last 35-day episode caused home sales to ebb, though they rebounded afterward.

The shutdown directly affects some transactions because the National Flood Insurance Program stops issuing new policies. The majority of home sales should be unaffected, but others may face potential delays due to limited staffing at various agencies. And while it’s tough to measure, the shutdown is likely a drag on consumer confidence.

One key pain point is the lack of new data. The September employment report, slated for Friday, has been delayed, so we don’t know how hiring and unemployment trended officially in the past month. Private data showed softer hiring, and the August job turnover report showed hiring and separations in line with recent trends. This makes it harder for both markets and policymakers to assess what’s going on and position for what’s ahead.

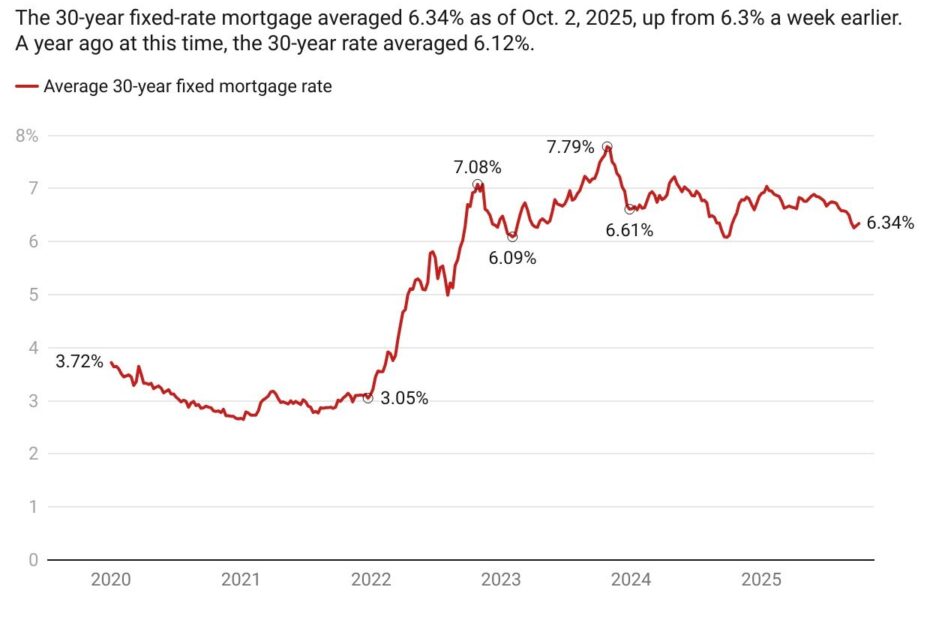

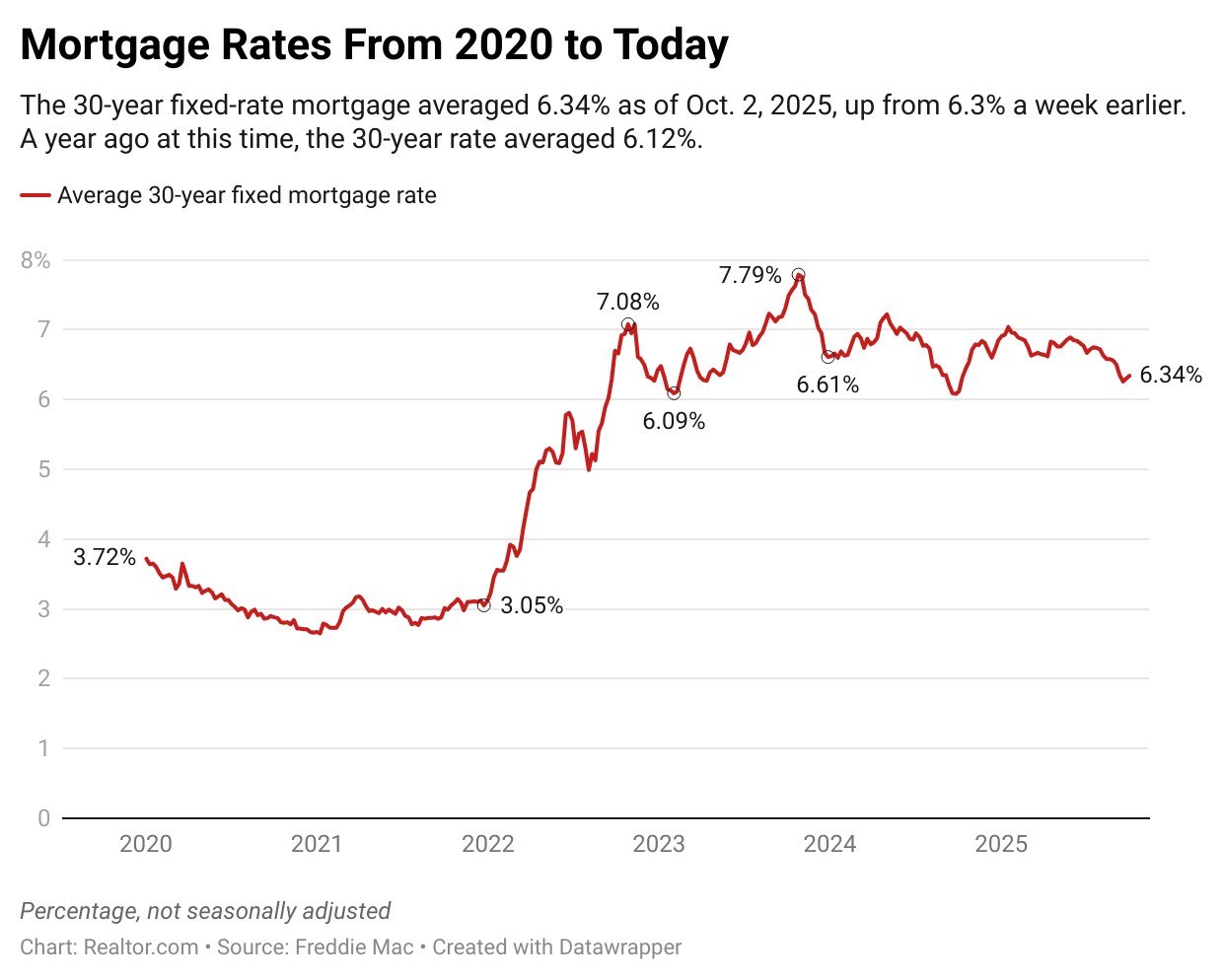

Mortgage rates edged up this week, but remain in the low 6% for a fourth week, as markets digest the shutdown and try to price in its impact. As mortgage rates have remained relatively high through most of 2025, home sales have remained low, and the rate on outstanding mortgage debt for homeowners has barely budged. In fact, 80% of homeowners with a mortgage still have a sub-6% rate.

Meanwhile, pending home sales picked up in August as buyers reacted to the dip in mortgage rates. A slower pace of home price growth undoubtedly improved affordability as well.

Realtor.com® September housing data suggests that price softness has largely continued, with listing prices holding flat and price cuts up compared to last year. Digging deeper, we find that price cuts are more common in lower price tiers nationwide and are rarer among million-dollar-plus homes. These trends are generally, but not universally, true at the local level, too, suggesting that both affordability and regional trends are likely drivers of this pattern.

Weekly housing data underscores price stability and also highlights a loss of selling momentum, with new listings declining and active listing growth slowing.

As we approach the Best Time To Buy nationwide, some markets are already there, with areas like Atlanta, Austin, TX, and Chicago wrapping up their best week as Las Vegas stands out for prime conditions next week.

Finally, you’ll probably know it when you see it, but what is a luxury home? And what’s the dividing line between merely high-end and ultra-luxury?

We dug into the data to see how the definition of luxury has evolved. The entry-luxury threshold is now over a million dollars nationwide, or roughly three times the current median home price. High-end luxury starts at $2 million, while ultraluxury starts above $5 million—each many multiples of the typical home price.