On the eve of the largest transfer of wealth in history, something is wrong: The heirs are missing.

Today, as many as 15.2 million adults ages 55 and older are childless, according to the latest estimate available from the U.S. Census Bureau. Of these adults, about 40% live alone—double the rate of similarly aged adults with children.

“We’re kind of in a troubling situation,” Ronald Lee, a UC Berkeley demographer and economist, tells Realtor.com®. “We’re stuck with these values and institutions that haven’t really adjusted to the fact that we live much longer and we’re having many fewer kids.”

That’s creating a historic paradox: On the one hand, $19 trillion in baby boomer home equity is preparing to move. On the other, the vertical flow of family legacy is being rerouted laterally to nieces, nephews, charities, and the high cost of the American health care system.

That introduces a slew of questions for the population, and uniquely, the housing market.

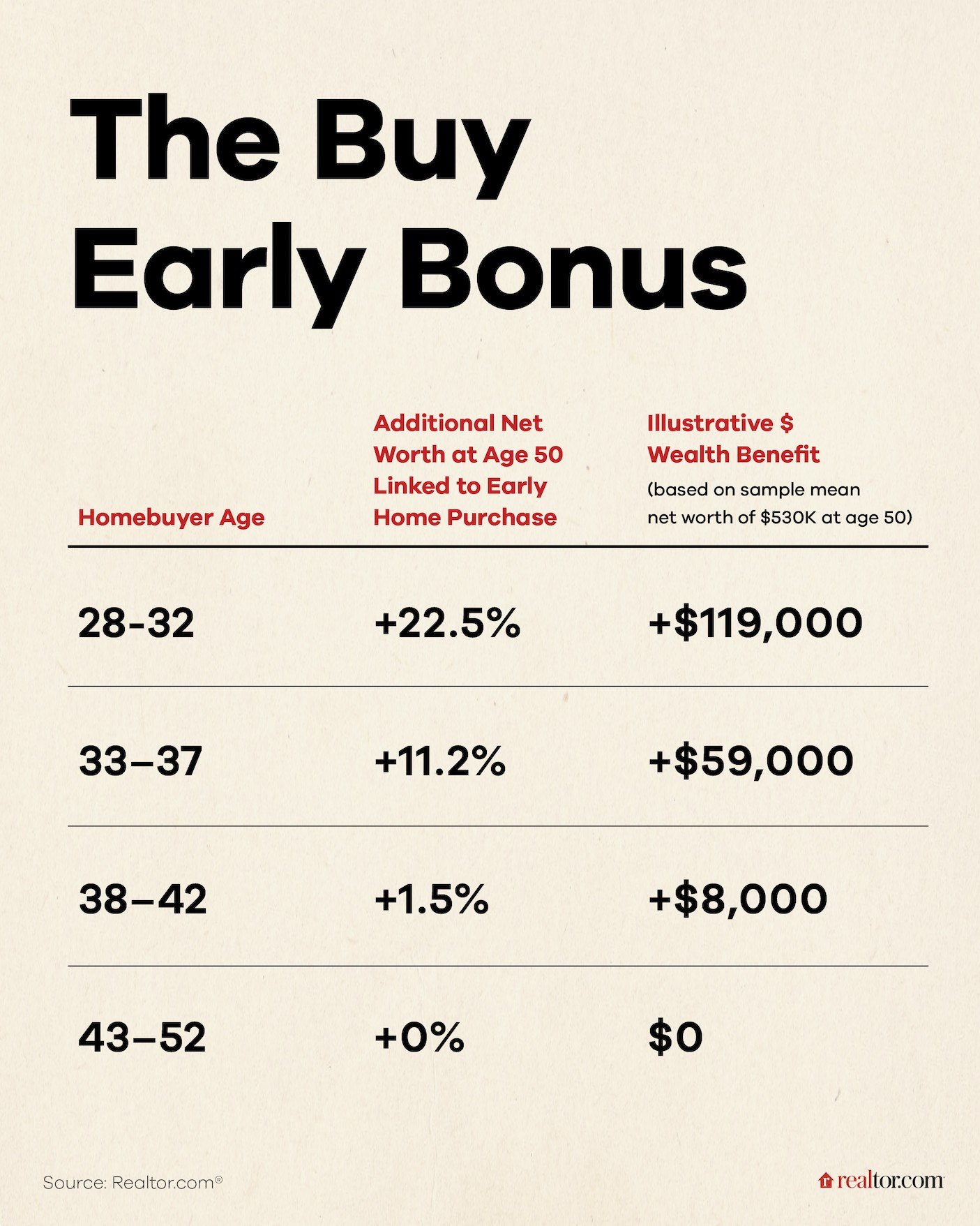

As steep competition has put more pressure on the role of family help for younger house hunters to become homeowners, children raised in homeowner households are 18.4 percentage points more likely to become homeowners by age 35, according to a Realtor.com analysis of data from the Panel Study of Income Dynamics.

So as the Great Wealth Transfer collides with the baby bust, the $124 trillion question is what happens to the American dream when the ladder of inheritance runs out of rungs?

The rise of ‘solo agers’ and ‘orphan-elders’

“There’s so many of us that are growing older without family support and structure,” Carol Marak, a financial educator who is aging on her own at 74 years old, tells Realtor.com. “I initially started out just wanting to build awareness about this, but it’s going to take more than building awareness. We need to put systems in place.”

In her work, she leads peer groups and workshops with other solo-agers to help them plan for the later stages of life. That includes financial, health care, and estate planning as well as social networking.

“We all have our own preferences for how we want to age, how we want to live, how we want to address these issues. I give [solo-agers] the tools for how to start thinking through these issues,” she says.

When asked where most of the solo-agers she works with plan on leaving their wealth, Marak says that many “don’t really care where it goes.”

“Most of us will leave it to a charity,” she adds, also citing nieces and nephews, as well as caretakers of beloved pets.

Some heirs may get more—but fewer people may benefit

As wealth moves laterally, it upends what Jay Zigmont, a certified financial planner who specializes in working with child-free clients, calls the “traditional life script.”

This script assumes a vertical flow: You build wealth and pass it on to direct heirs.

Baby boomers alone are estimated to transfer roughly $84 trillion in wealth through 2048, with millennials standing to inherit the lion’s share, according to projections from Cerulli Associates.

But as families shrink, that flow is narrowing and colliding with a long and established trend of wealth inequality.

“Since there are fewer children, that means for each old person, those inherited assets are going to be concentrated on a smaller number of people,” Lee explains.

So instead of spreading, wealth is at risk of pooling—more than it already is. Cerulli’s estimates suggest that 2% of households will control over 50% of the Great Wealth Transfer’s transfers. Add in fewer people (or just one person) to divide the assets among and the individual lift can be massive.

Zigmont describes one 29-year-old client whose inheritance from her grandmother was so significant “she doesn’t have to work again in her life.”

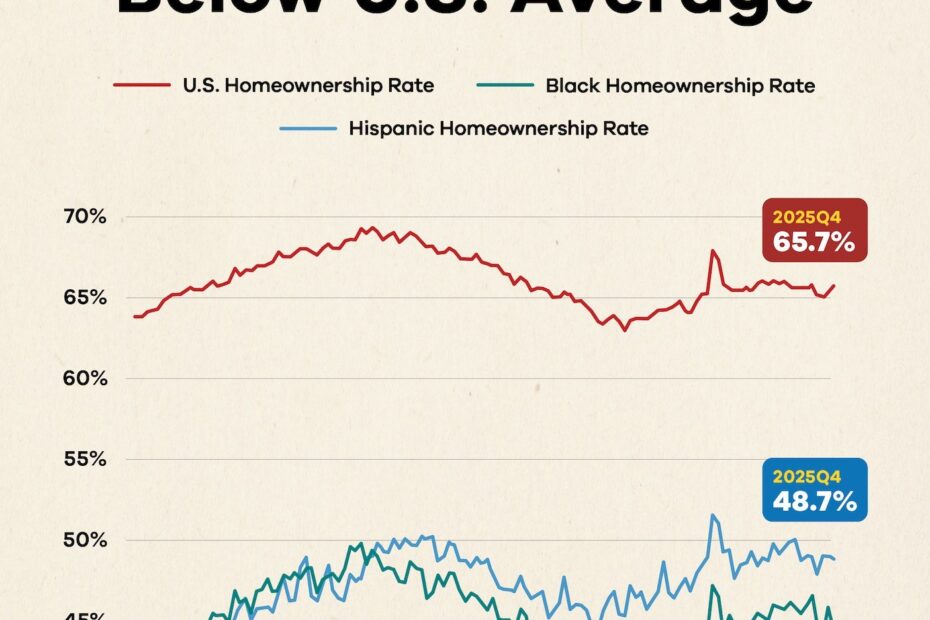

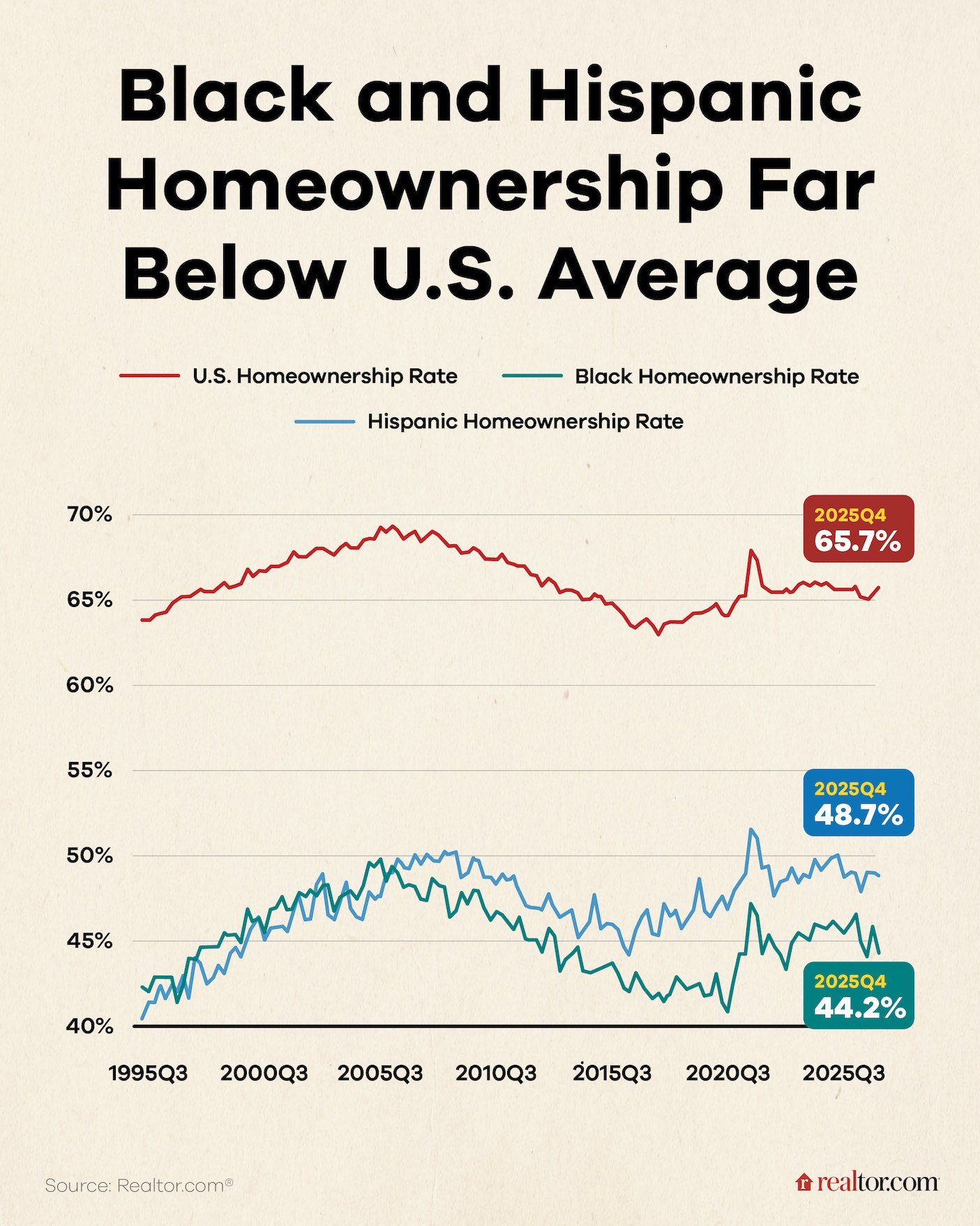

That concentration risks super-charging long entrenched wealth divides. Today, the homeownership rate for white households is 75.1%, compared with 44.2% for Black households and 48.7% for Hispanic households.

Even for the lucky heirs, the timing is at risk of being a mismatch. As people live longer, they’re bequeathing wealth to their inheritors later.

“The age of inheriting is going to be in the 50s, something like that,” Lee says—long after the critical window where buying a home can maximize a person’s lifetime net worth. “It comes too late to really help you with your life.”

Long-term care may be the biggest heir of all

Even when there is significant wealth to pass on, there is no guarantee that it will survive the high cost of aging.

As of 2026, the nationwide average annual cost for a shared room in a nursing home has climbed to roughly $120,000, while private rooms now exceed $136,000, according to the American Council on Aging.

It’s a sum few can afford out of pocket; and for those with children, the gap is often closed by familial care—an informal support system that costs adult children an estimated $144,000 to $201,000 over a two year period, according to one study.

But for those aging solo, that unpaid labor isn’t baked in. To make matters harder, there isn’t the same social safety net that there once was.

The problem, Lee explains, comes back to the changing population: Older generations are living longer with higher care needs and fewer younger workers to fund the programs that provide a backstop.

Lee’s research shows that public transfers like these (i.e., Social Security and Medicaid) historically play a larger role in high-income countries like the U.S. than any massive transfer of private wealth.

“The transfers older people get … are often the only thing standing between an elderly person and poverty,” he says.

This structural void is exactly what Marak recognized in her 50s.

While she owned her home outright, she realized she had little liquidity to fund the professional support she would eventually need as a solo-ager. To bridge that gap, she spent five years saving aggressively before selling her suburban house and downsizing to a high-rise in downtown Dallas, where she’s closer to public transit, her doctors, and community.

Her goal—a lesson she now imparts to her senior groups—is to maximize quality of life while ensuring her money outlasts her. In this new landscape, leaving wealth behind isn’t about ensuring a windfall for an heir; it is a final level of financial security that guarantees these seniors will be taken care of.